[ad_1]

Legendary fund supervisor Li Lu (who Charlie Munger backed) as soon as mentioned, ‘The largest funding threat just isn’t the volatility of costs, however whether or not you’ll endure a everlasting lack of capital.’ So it is perhaps apparent that you have to contemplate debt, when you concentrate on how dangerous any given inventory is, as a result of an excessive amount of debt can sink an organization. As with many different corporations Tamil Nadu Newsprint and Papers Restricted (NSE:TNPL) makes use of debt. However is that this debt a priority to shareholders?

When Is Debt Harmful?

Debt and different liabilities develop into dangerous for a enterprise when it can’t simply fulfill these obligations, both with free money stream or by elevating capital at a lovely worth. Finally, if the corporate cannot fulfill its authorized obligations to repay debt, shareholders might stroll away with nothing. Nevertheless, a extra traditional (however nonetheless costly) scenario is the place an organization should dilute shareholders at an inexpensive share worth merely to get debt underneath management. By changing dilution, although, debt might be an especially good device for companies that want capital to put money into development at excessive charges of return. Step one when contemplating an organization’s debt ranges is to think about its money and debt collectively.

View our latest analysis for Tamil Nadu Newsprint and Papers

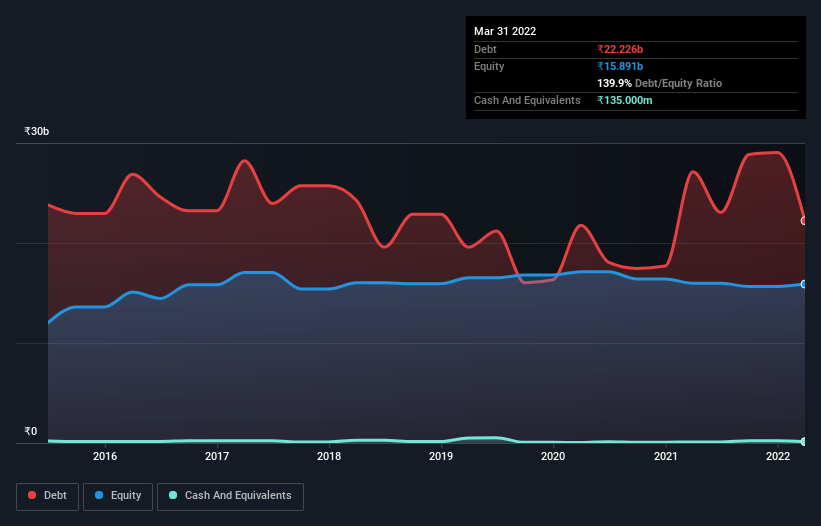

What Is Tamil Nadu Newsprint and Papers’s Debt?

The picture under, which you’ll click on on for better element, reveals that Tamil Nadu Newsprint and Papers had debt of ₹22.2b on the finish of March 2022, a discount from ₹27.1b over a 12 months. And it would not have a lot money, so its internet debt is about the identical.

How Wholesome Is Tamil Nadu Newsprint and Papers’ Steadiness Sheet?

In keeping with the final reported stability sheet, Tamil Nadu Newsprint and Papers had liabilities of ₹21.9b due inside 12 months, and liabilities of ₹19.9b due past 12 months. Offsetting these obligations, it had money of ₹135.0m in addition to receivables valued at ₹2.75b due inside 12 months. So its liabilities whole ₹39.0b greater than the mix of its money and short-term receivables.

This deficit casts a shadow over the ₹12.7b firm, like a colossus towering over mere mortals. So we undoubtedly assume shareholders want to look at this one carefully. In any case, Tamil Nadu Newsprint and Papers would doubtless require a serious re-capitalisation if it needed to pay its collectors right this moment.

We use two major ratios to tell us about debt ranges relative to earnings. The primary is internet debt divided by earnings earlier than curiosity, tax, depreciation, and amortization (EBITDA), whereas the second is what number of occasions its earnings earlier than curiosity and tax (EBIT) covers its curiosity expense (or its curiosity cowl, for brief). The benefit of this strategy is that we consider each absolutely the quantum of debt (with internet debt to EBITDA) and the precise curiosity bills related to that debt (with its curiosity cowl ratio).

Weak curiosity cowl of 0.83 occasions and a disturbingly excessive internet debt to EBITDA ratio of 6.2 hit our confidence in Tamil Nadu Newsprint and Papers like a one-two punch to the intestine. The debt burden right here is substantial. Nevertheless, it must be some consolation for shareholders to recall that Tamil Nadu Newsprint and Papers really grew its EBIT by a hefty 142%, during the last 12 months. If that earnings pattern continues it is going to make its debt load way more manageable sooner or later. The stability sheet is clearly the realm to concentrate on if you end up analysing debt. However it’s Tamil Nadu Newsprint and Papers’s earnings that can affect how the stability sheet holds up sooner or later. So when contemplating debt, it is undoubtedly price wanting on the earnings pattern. Click here for an interactive snapshot.

Lastly, a enterprise wants free money stream to repay debt; accounting earnings simply do not reduce it. So we all the time test how a lot of that EBIT is translated into free money stream. Over the past three years, Tamil Nadu Newsprint and Papers generated free money stream amounting to a really sturdy 88% of its EBIT, greater than we would anticipate. That positions it properly to pay down debt if fascinating to take action.

Our View

To be frank each Tamil Nadu Newsprint and Papers’s curiosity cowl and its monitor document of staying on high of its whole liabilities make us somewhat uncomfortable with its debt ranges. However on the brilliant aspect, its conversion of EBIT to free money stream is an effective signal, and makes us extra optimistic. As soon as we contemplate all of the components above, collectively, it appears to us that Tamil Nadu Newsprint and Papers’s debt is making it a bit dangerous. Some folks like that kind of threat, however we’re conscious of the potential pitfalls, so we would in all probability desire it carry much less debt. There is no doubt that we study most about debt from the stability sheet. Nevertheless, not all funding threat resides inside the stability sheet – removed from it. Bear in mind that Tamil Nadu Newsprint and Papers is showing 3 warning signs in our investment analysis , and a pair of of these should not be ignored…

If, in spite of everything that, you are extra keen on a quick rising firm with a rock-solid stability sheet, then take a look at our list of net cash growth stocks immediately.

Have suggestions on this text? Involved concerning the content material? Get in touch with us immediately. Alternatively, electronic mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is normal in nature. We offer commentary based mostly on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles usually are not meant to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your aims, or your monetary scenario. We purpose to deliver you long-term targeted evaluation pushed by basic knowledge. Notice that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link