[ad_1]

It is common for a lot of buyers, particularly those that are inexperienced, to purchase shares in corporations with story even when these corporations are loss-making. However as Peter Lynch mentioned in One Up On Wall Avenue, ‘Lengthy photographs virtually by no means repay.’ Loss-making corporations are at all times racing towards time to succeed in monetary sustainability, so buyers in these corporations could also be taking up extra threat than they need to.

So if this concept of excessive threat and excessive reward would not swimsuit, you may be extra keen on worthwhile, rising corporations, like BLB (NSE:BLBLIMITED). Now this isn’t to say that the corporate presents the perfect funding alternative round, however profitability is a key element to success in enterprise.

View our latest analysis for BLB

How Quick Is BLB Rising Its Earnings Per Share?

Sturdy earnings per share (EPS) outcomes are an indicator of an organization reaching strong income, which buyers look upon favourably and so the share value tends to replicate nice EPS efficiency. Which is why EPS development is seemed upon so favourably. Commendations should be given in seeing that BLB grew its EPS from ₹0.21 to ₹1.78, in a single quick 12 months. Whereas it is troublesome to maintain development at that degree, it bodes properly for the corporate’s outlook for the long run.

High-line development is a good indicator that development is sustainable, and mixed with a excessive earnings earlier than curiosity and taxation (EBIT) margin, it is an effective way for a corporation to keep up a aggressive benefit out there. It is famous that BLB’s income from operations was decrease than its income within the final twelve months, so that might distort our evaluation of its margins. Whereas BLB might have maintained EBIT margins during the last 12 months, income has fallen. Whereas this will increase considerations, buyers ought to examine the reasoning behind this.

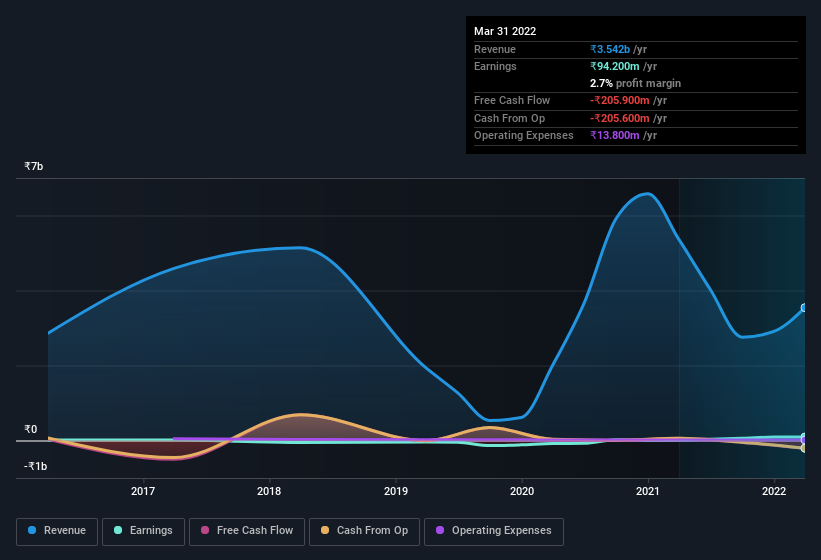

You may check out the corporate’s income and earnings development development, within the chart beneath. For finer element, click on on the picture.

Since BLB isn’t any large, with a market capitalisation of ₹830m, you need to definitely check its cash and debt earlier than getting too enthusiastic about its prospects.

Are BLB Insiders Aligned With All Shareholders?

Seeing insiders proudly owning a big portion of the shares on subject is usually signal. Their incentives will probably be aligned with the buyers and there is much less of a chance in a sudden sell-off that might impression the share value. So we’re happy to report that BLB insiders personal a significant share of the enterprise. Actually, they personal 72% of the corporate, so they’ll share in the identical delights and challenges skilled by the atypical shareholders. Instinct will inform you it is a good signal as a result of it suggests they are going to be incentivised to construct worth for shareholders over the long run. In fact, BLB is a really small firm, with a market cap of solely ₹830m. So regardless of a big proportional holding, insiders solely have ₹595m price of inventory. Which may not be an enormous sum nevertheless it ought to be sufficient to maintain insiders motivated!

Is BLB Value Conserving An Eye On?

BLB’s earnings per share have been hovering, with development charges sky excessive. This degree of EPS development does wonders for attracting funding, and the big insider funding within the firm is simply the cherry on high. The hope is, after all, that the robust development marks a basic enchancment within the enterprise economics. So based mostly on this fast evaluation, we do suppose it is price contemplating BLB for a spot in your watchlist. Nonetheless, earlier than you get too excited we have found 3 warning signs for BLB (1 is probably critical!) that you ought to be conscious of.

Though BLB definitely appears good, it might attraction to extra buyers if insiders had been shopping for up shares. In the event you prefer to see insider shopping for, then this free list of growing companies that insiders are buying, could possibly be precisely what you are on the lookout for.

Please observe the insider transactions mentioned on this article confer with reportable transactions within the related jurisdiction.

Have suggestions on this text? Involved concerning the content material? Get in touch with us straight. Alternatively, e-mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is basic in nature. We offer commentary based mostly on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles will not be meant to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary state of affairs. We goal to carry you long-term targeted evaluation pushed by basic knowledge. Notice that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link