[ad_1]

simarts/iStock Editorial by way of Getty Pictures

Lots has occurred since my final article on the 20th of April. The financial institution revealed excellent earnings results, which made the shares rebound considerably. Nevertheless, after that, the monetary markets had been fairly wired due to the Fed’s hawkish rhetoric and the ECB’s resolution to lift the rates of interest. This made the monetary markets shatter. Though larger rates of interest normally imply larger income for the monetary sector, banking shares are extra delicate than the general market. In different phrases, banks are extremely cyclical and don’t do effectively throughout recessions. On the identical time, UBS (NYSE:UBS) is an undervalued worthwhile financial institution and its inventory ought to ultimately get well. Let me clarify this in some extra element.

The financial institution’s monetary outcomes

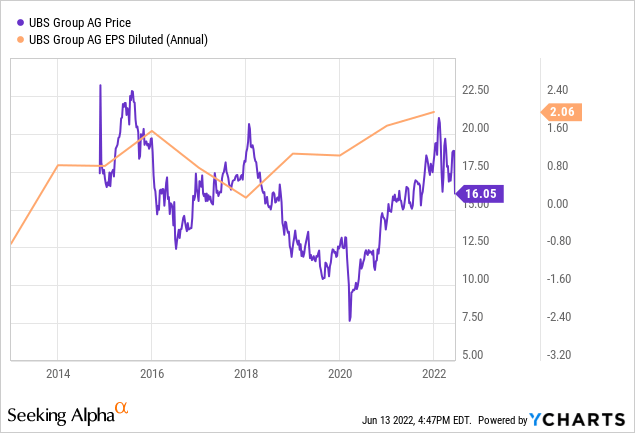

Between 2012 and 2018 the financial institution’s quarterly outcomes didn’t present secure development. Nevertheless, between 2018 and 2022 the financial institution confirmed sound earnings per share (EPS) development however the inventory value didn’t comply with. As might be seen from the graph beneath, the start of 2020 was a good time to purchase the inventory.

The identical might be mentioned concerning the final earnings outcomes, revealed on the finish of April.

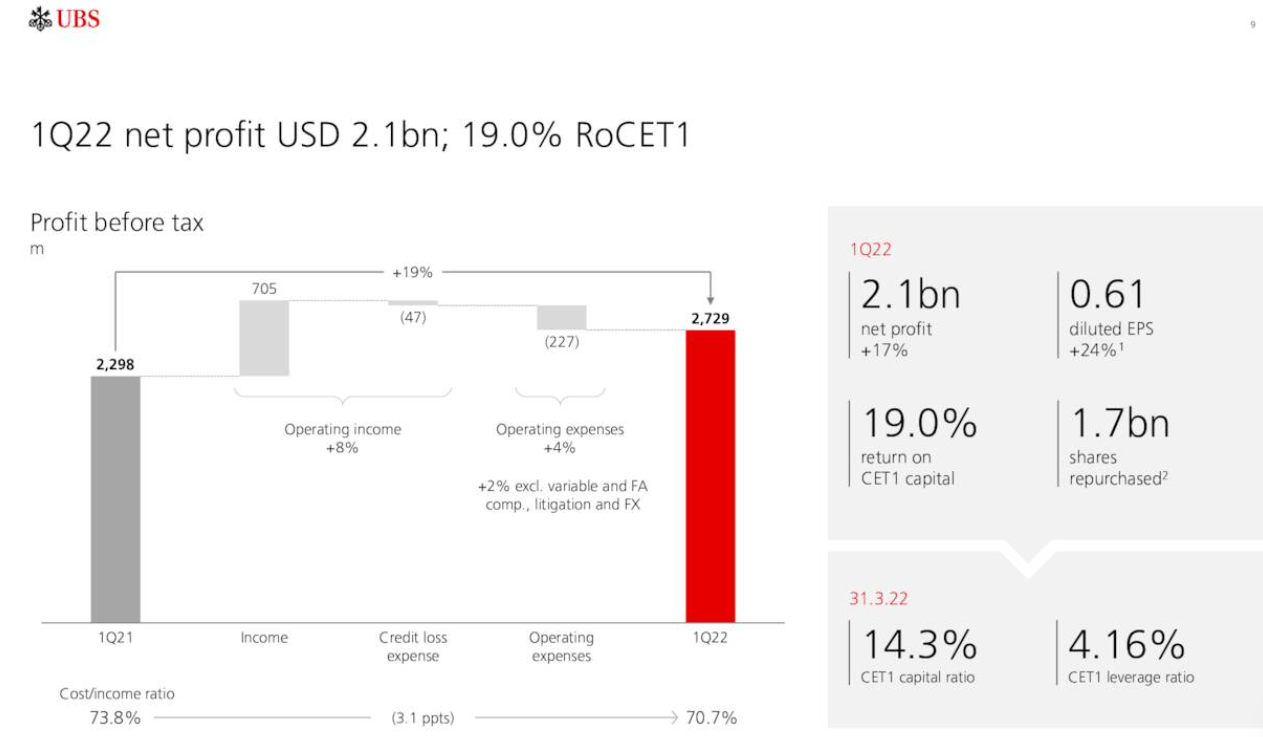

A lot of monetary indicators reported for the primary quarter of 2022 had been actually good. For instance, the CET 1 capital ratio for 1Q2022 was 14.3%, whereas the requirement is 10%. The return on CET1 capital was 19%, which is kind of sound given the financial institution’s excessive CET1.

The financial institution’s earnings presentation, slide 10

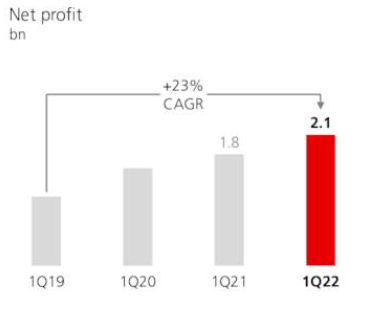

However crucial growth for 1Q2022 was the web revenue determine of $2.1 billion. By itself it might not imply as a lot but when we have a look at the web revenue historical past for the final 4 years, we are going to see there was substantial development. The web revenue rose from $1.8 billion in 1Q2021 to $2.1 billion in 2Q2022, an virtually 17% rise. That’s fairly spectacular, given the financial institution’s conservative profile.

UBS earnings presentation

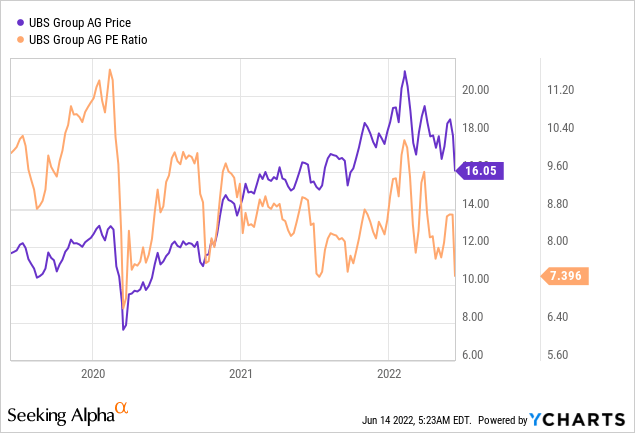

Allow us to assume the financial institution reviews precisely the identical revenue for every of the next three quarters. So, $2.1 billion instances 4 offers us $8.4 billion. The present market capitalisation is round $60 billion. If we divide the present market capitalisation by $8.4 billion, we are going to get a price-to-earnings (P/E) ratio of seven.14, which isn’t excessive in any respect.

In truth, if we take a look on the graph above, the financial institution’s P/E ratio is now hovering close to its 3-year lows. The present indicator is simply barely larger than the spring 2020 low of about 6.5. The latter was logical on the time because the international pandemic made many nations’ economies halt. So, the inventory markets crashed. Proper now there may be additionally a purpose for the inventory value lower, specifically because of the central banks’ financial insurance policies.

The central banks’ financial insurance policies

The Fed, the ECB and even the Swiss National Bank are sounding the alarm – the inflation indicators are close to their multi-year highs. The ECB and the Fed have already began elevating the rates of interest. The Swiss Nationwide Financial institution additionally determined to lift the rates of interest. This has not occurred for years since in Switzerland the inflation charge is historically very low and even unfavourable.

Financial tightening is, usually talking, bearish for the worldwide financial system because it normally provokes recessions. The banking sector can also be extremely cyclical and is affected by the macroeconomic circumstances. Nevertheless, we will additionally safely say that, supplied there isn’t any recession, rising rates of interest ought to elevate the monetary sector’s curiosity revenue – revenue from borrowing and lending. So, it actually is determined by the place the financial system is heading subsequent. However, UBS isn’t a really commonplace financial institution, in that sense.

UBS as a financial institution

As a financial institution UBS wouldn’t lose a lot even when there’s a severe recession. Right here, I don’t even trace on the truth the Swiss authorities got here to the rescue of UBS when there was the 2008-2009 disaster, additionally affecting Switzerland. After the disaster the UBS modified their threat profile and have become extra conservative than they was once. That’s logical since UBS is a financial institution for the wealthy. In different phrases, it doesn’t rely an excessive amount of on lending cash to extremely indebted people and companies.

That could be a nice constructive for UBS – in different phrases, it might not endure from its shoppers’ bankruptcies to the extent its friends would, because it doesn’t have dangerous shoppers.

Though I have no idea precisely when this correction would finish and if there’s a recession any time quickly, in my opinion, shopping for UBS at a reduction would make excellent sense since it’s “recession-resistant”.

Technical evaluation

By all means, technical evaluation is simply secondary to the basic one. Nevertheless, I made a decision to conduct some evaluation utilizing Bollinger bands.

In different phrases, the financial institution’s inventory value strikes inside sure bands or strains. It’s in a sure development. Proper now the 5-year development appears to be upward. There’s some volatility and data noise over the way in which however general the development stays intact.

TradingView

On the graph above since 2020 there may be an upward transfer of the financial institution’s inventory value. Offered there isn’t any recession within the subsequent a number of month or some other important monetary misery, UBS inventory value would preserve rising and traders would do effectively in the event that they purchase when there may be “blood on the streets”.

For my part, it isn’t a good suggestion to speculate when the inventory market indices are at their all-time highs and monetary mass media advocate energetic investing. Simply the alternative is true – it’s the finest to purchase sound corporations’ shares after their correction when every thing else is crashing. UBS has not confronted any important scandals within the final a number of years, has reported wonderful income however its inventory corrected considerably through the market unload.

Conclusion

UBS is a extremely worthwhile financial institution for the wealthy working in a cyclical sector. Its inventory received cheaper primarily because of the data noise. Offered there isn’t any recession within the subsequent a number of months, the inventory has nice upward potential within the close to future. Technical evaluation suggests a powerful upward development. It’s the finest to spend money on worthwhile banks when every thing is promoting at a reduction.

[ad_2]

Source link