[ad_1]

Rixipix/iStock through Getty Photos

“You mentioned earlier than you had been ready for an indication. What signal are you ready for?” – Egon Spengler, Ghostbusters

It’s a on condition that swift financial tightening will proceed over the summer time months because the Fed prepares to rein in inflation that’s operating close to a 40-year excessive. The current CPI print is one other knowledge level that’s essential to expectations of Fed actions. Finally if inflation goes to gradual commodities must cease going up. WTI Crude stays on the $110/barrel stage. and Nat Gasoline is simply off the highs for the yr. Close to-term inflation doesn’t appear to be decelerating, and commodities are going to have to return down sustainably for that to happen. The issue is they could begin retreating from highs due to a world slow-down.

Charge expectations are quickly adjusting, with the market now pricing in a 3.5%-4% Fed funds charge at year-end, up from an anticipated 0.75% charge on the finish of final yr. Whereas the Fed simply began quantitative tightening on June 1 and has solely delivered comparatively small charge hikes so far, it’s clear that expectations of aggressive Fed tightening are taking some wind out of the sails of the inventory market and the economic system.

We have seen among the most interest-rate-sensitive areas of the economic system, resembling housing, are slowing as evidenced by mortgage buy functions falling to a four-year low. Sentiment has additionally fallen sharply, with client, enterprise, and investor sentiment now sitting at ALL-TIME lows. The Fed has a fragile balancing act to chill demand with out tipping the economic system right into a recession, and the inventory market is within the technique of re-pricing this new backdrop. Given the current value motion, market members are leaning towards a worst-case state of affairs.

The chance that the Fed engineers a “soft-landing” must be based mostly on the resiliency of the patron, notably as client spending makes up ~70% of the economic system. So far, client spending has held up properly within the face of rising costs and elevated asset volatility, however how far more can the patron soak up?

We noticed a “Goldilocks” jobs quantity for Might however thus far there was no job progress. There are nonetheless fewer individuals employed at present than earlier than the pandemic. Might jobs knowledge was a bit stronger than anticipated in mixture, although common hourly earnings had been a bit softer, and labor participation elevated properly.

Client Is In Good Form

Excessive inflation is leaving its mark on the typical client however they’re in a a lot better place to attempt to climate this storm. Client steadiness sheets have not often been in higher form. Strong job positive aspects, robust wage progress, and a major quantity of collected financial savings for the reason that pandemic started to proceed to offer loads of hearth energy to assist consumption. Shoppers additionally used the pandemic to pay down debt. Family debt servicing ratios at the moment are operating at a 40-year low, considerably under the degrees seen in the course of the three prior recessions. This means that buyers can enhance their debt-financing choices (i.e., bank cards), if wanted, to keep up their spending.

On that observe, there’s some proof that financial savings are being spent down. Client debt ranges relative to GDP rose sequentially in Q1 after a considerable decline; revenue progress is operating under spending progress, so it isn’t a shock that money balances should not rising anymore and households are beginning to tackle debt.

It isn’t the identical image we noticed earlier than the monetary disaster. Housing-related debt is simply 30% of the worth of housing-related belongings; that is the very best fairness share of family actual property publicity in over a technology and exhibits how robust family belongings are relative to liabilities. Even with booming curiosity within the housing market, mortgage debt is lower than half of GDP and is continuous to pattern decrease. Whereas the typical client is at a greater place to begin they’re getting hit by a two-pronged assault.

The wealth impact is being eroded, whereas inflation is consuming away at their buying energy. If that scene lingers, your entire “robust client” argument goes by the wayside.

Company Scene

Items-producing firms had been huge beneficiaries in the course of the pandemic as individuals spent cash on issues they might get pleasure from at dwelling, resembling furnishings, electronics, and different at-home devices. Nonetheless, because the economic system has reopened, individuals have shifted their spending to extra services-related objects, resembling airline journey and restaurant spending. Whereas this shift was predictable, some “big-box” retailers have reported elevated stock ranges and slowing gross sales which have raised issues concerning the well being of the patron.

The entire real-time exercise metrics affirm shoppers are spending on providers as restaurant bookings, lodge occupancy and TSA screenings are all at or close to post-pandemic highs. In reality, with over 80% of shoppers planning to take a summer time trip this yr, many airways/cruise strains have raised their ahead gross sales steerage because of the elevated demand. This shift shall be supportive of financial progress as providers spending makes up ~60% of complete client spending and stays under its pre-pandemic pattern.

All of that bodes properly within the very close to time period. So it goes again to the sooner discussions of how lengthy inflation lasts at these ranges. That can decide how lengthy can the patron deal with larger costs. Buyers will stay hyper-sensitive to inflationary knowledge factors shifting ahead, as its trajectory ends in a variety of potential outcomes over the approaching months. That makes any close to/intermediate-term market forecast that has any conviction behind it practically inconceivable.

A comfortable touchdown is essential to the market. Why? As a result of following the three different durations that the Fed has engineered a comfortable touchdown (1965, 1984, and 1994), the S&P 500 was up ~15% on an annualized foundation over the subsequent three years and was optimistic every time.

When a recession is concerned all bets are off, as losses may mount up shortly. Sure, regardless of the weak point recently a full-blown recession is not priced into this market. There are numerous shifting elements to this “story” and one of many largest is the half Power prices play within the inflation scene. If the united stateseconomy stays considerably resilient, and the Chinese language economic system rebounds after the entire COVID roadblocks it’s onerous to think about crude oil collapsing to the purpose the place inflation slows dramatically or disappears in a single day. There are different elements at work that can preserve costs elevated.

Power

The European Union’s embargo in opposition to Russian oil, initially proposed in early Might, was confirmed just lately at a political stage. The laws nonetheless should be finalized by the European Fee, and the implementation timetable extends to the top of 2022. What we all know already is that pipeline deliveries is not going to be restricted, a minimum of within the preliminary stage. The embargo will apply to seaborne (tanker) deliveries. By the use of background, roughly 4 million barrels per day of pre-war Russian exports had been offered to EU nations, of which 75% had been seaborne.

A query that is still up for dialogue is whether or not the EU will ultimately impose what’s often called secondary sanctions in opposition to non-European firms which might be nonetheless transport or buying Russian oil. Secondary sanctions would purpose to stop Russia from counting on China, India, Turkey, or different nations as proverbial “reduction valves” for oil exports. Ordinarily, the oil market’s inherent fungibility implies that Russia can promote with out restrict to jurisdictions with out sanctions of their very own, however secondary sanctions would impede that.

Whereas an finish to this depressing conflict in Ukraine will trigger a knee-jerk response to the vitality and fairness markets, does anybody imagine the world will open its arms up and embrace “Something Russian”? So it appears uncertain that an finish to the conflict will get Russian oil again into the combination. It’s incumbent for the U.S. to step up manufacturing to assist with the shortfall.

After all, the opposite state of affairs is a world recession that kills demand and the worth of Oil will even be killed together with fairness markets.

That state of affairs is also referred to as being between a “Rock and a Exhausting Place”.

Meals For Thought

Talking of somebody who’s between a rock and onerous place The White Home has introduced that president Biden shall be taking a visit to Saudi Arabia to speak about points, like “oil manufacturing”. One has to marvel if they will remember that they were called a “pariah” by Mr. Biden in 2020. It is fascinating that drilling for oil in the united statesis not acceptable in a world that’s obsessive about international local weather change, BUT completely acceptable if the drilling takes place in Saudi Arabia or elsewhere on the earth.

Whereas the strategy to fixing HIGH vitality prices requires a visit to the Saudis, the “jihad” in opposition to the oil trade that started in January 2021 continues.

That was one of many current salvos fired by the administration on the oil trade.

Exxon (XOM) determined to answer to the accusations by citing what I wish to see FACT as a substitute of spin.

We (Exxon) elevated manufacturing within the Permian Basin by 70%, or 190,000 barrels per day, between 2019 and 2021. We count on to extend manufacturing from the Permian by one other 25% this yr. We’re spending 50% extra in capital expenditures within the Permian in 2022 vs 2021 and are growing refining capability to course of U.S. mild crude by about 250,000 barrels per day – which is the equal of including a brand new medium sized refinery.

We reported losses of greater than $20 billion in 2020, and we borrowed greater than $30 billion in 2019 and 2020 to assist our investments in manufacturing all over the world. In 2021, complete taxes on the corporate’s revenue assertion had been $40.6 billion, a rise of $17.8 billion from 2020.

That does not embody native and state taxes.

The anti-business local weather will proceed to have unfavorable ramifications for the economic system and the inventory market.

Now it seems there’s but extra anti-capitalist rhetoric that would change the vitality scene for buyers. After I hear the administration chastise the oil trade and announce that above-normal profits for the “refiners” are unacceptable it is time to notice there’s NO likelihood of a coverage change regardless of the continuing “disaster”. This commentary resurfaces the nonsensical windfall revenue tax proposal, that if enacted will KILL drilling and refining within the U.S.

The administration deems it essential to depend on “others” to repair the vitality disaster. The tip recreation may simply be a deep international recession that would be the deciding issue bringing vitality prices down.

World Markets

The STOXX 600 closed at 52-week lows this week much like these of the S&P 500, having collapsed over the previous week in a world response to US inflation. Issues aren’t wanting any higher within the UK the place a unfavorable Q2 GDP print appears to be like doubtless amidst an enormous cost-of-living shock that has the Financial institution of England virtually explicitly engineering a recession and housing market collapse amidst a possible commerce conflict per week after the unpopular Prime Minister survived a celebration no-confidence vote.

In brief: in Europe, nearly all the things is down and at 52-week lows.

It is a totally different story in China. The Chinese language market as measured by the CSI 300 (ASHR) posted its third consecutive week of positive aspects. The China 25 Index ETF (FXI) broke its 5-week profitable streak by posting a modest loss for the week.

The Week On Wall Road

Getting into per week the place the Fed was set to proclaim their subsequent transfer on rates of interest and buyers had been buckling up for a quadruple witching on Friday. They knew each occasions would preserve uncertainty elevated many had no concept how volatility was about to ramp larger. Markets had been already weak, with the S&P having posted losses in 9 of the final 10 weeks. The stage was set.

The S&P opened, then remained in “official” BEAR market territory (-20% from the highs) till the closing bell. The truth that the S&P 500 closed down 20% does not inform us something that we do not already know based mostly available on the market motion during the last a number of months, however merely makes the S&P 500’s BEAR market ‘official’.

It wasn’t a fairly image for danger belongings of any variety as international markets had been down over 2+%. Treasuries offered off onerous, and crypto costs crashed. Issues over inflation and its influence on financial progress have develop into heightened during the last a number of days, and in contrast to prior durations in current historical past the place progress has come into query, with inflation pressures as robust as they’re, there’s little optimism that the Fed might help to cushion the blow.

The S&P fell 3.8% closing at 3749, which was important as a result of the index breached the Might Lows. Monday was the fourth straight lack of 1% or extra, one thing the market hasn’t completed since Christmas Eve of 2018. This was additionally the third straight lack of 2% or extra, a streak that hasn’t been examined since August of 2015. That was the final time the market skilled a “progress” scare. Because it turned out that scare was extra of a conjured-up state of affairs, whereas at present’s points are certainly REAL.

Solely 5 shares in your entire S&P 500 had been inexperienced on the day and never a single NYSE working firm hit a brand new 52-week excessive (the second day in a row with zero new highs). Not solely was it a 90% draw back day, nevertheless it additionally was one of the crucial excessive ones we are going to ever see. 98.3% of shares declined, on 98.6% of the quantity, and 99.9% of the factors traded. The S&P 500 has now fallen 10% in simply 4 classes, as now we have gone from impartial readings to draw back extremes in a rush.

Not a lot modified on Tuesday. One other day, one other contemporary new intraday low because the promoting continued. Wednesday noticed rates of interest rise together with shares. The 7-day 9% waterfall decline ended with a knee-jerk bounce because the Fed’s rate of interest determination is out of the way in which. The S&P rose 1.4% and the entire different main indices posted positive aspects.

The post-Fed bounce was short-lived because the S&P 500 fell 3+%, greater than erasing all of Wednesday’s positive aspects. The 8-day decline reached 11%. It has been a one-step ahead and two steps backward marketplace for a while now, and the Wednesday/Thursday value motion was one other illustration of that sample.

Whereas the S&P went out on a optimistic observe to finish the week, it wasn’t sufficient to erase the weekly loss which tallied 4%. It was the worst week for the index since March 2020. That made it 10 out of the final 11 weeks the place the index has posted a loss. In that time-frame, the S&P is down 18+%.

The Fed

The Federal Reserve had foreshadowed 50 foundation level hikes in June and July, However current inflation knowledge pressured the difficulty and the FOMC hiked the Fed funds charge band by 75 foundation factors to 1.50%-1.75%. It’s the largest increase since November 1994. The assertion was relatively quick.

The Fed anticipates that “ongoing will increase within the funds charge shall be applicable, however with out giving any indication of the scale. The conflict in Ukraine was seen creating further pressures on costs whereas weighing on the worldwide economic system. The Fed mentioned it will likely be “ready to regulate the stance of financial coverage as applicable if dangers emerge that would impede the attainment of the Committee’s targets.”

The assertion added it is going to proceed to cut back its steadiness sheet as beforehand described. The vote was 10-1 with the one dissent coming from Mester, who analysts contemplate one of many extra hawkish. She most popular a 50 bp enhance. For my part slowing tightening (not to mention pausing) will not be tenable with inflation this excessive. A 3.5%-4% Fed Funds charge is a practical end result if something like the present inflation path continues, and ultimately, markets will begin to calm because the economic system strikes again in the direction of equilibrium. One factor is for certain: the present path for rates of interest is excessive. Over the past 9 months, 2-year observe yields are up 3.15%. That’s the most excessive change in two-year yields from 1994’s bond market carnage, which was 2.79 proportion factors over 9 months.

In brief, the present tightening is knocking on the doorways of the quickest tightening for the reason that Volcker shock within the early Nineteen Eighties.

The two% end-of-year inflation goal was lastly scrapped as Chair Powell now sees an end-of-year charge at round 5%. I used to be within the “it’s important to be kidding me camp” relating to the two% forecast now I’ve moved to the “present me” camp on the revised 5% forecast.

The FOMC is anticipating progress of practically 3% within the second half to get to their 1.7% annual advance estimate per their current Abstract of Financial Projections. That’s going to be virtually inconceivable with a slowing client, particularly contemplating the shock of value hikes in classes the place demand is very inelastic together with electrical energy, gasoline, and lease.

If the Fed is to be accused of something it is the actual fact they determined to “toe the social gathering line”, downplaying the severity of the state of affairs from transitory inflation to GDP progress.

The Economic system

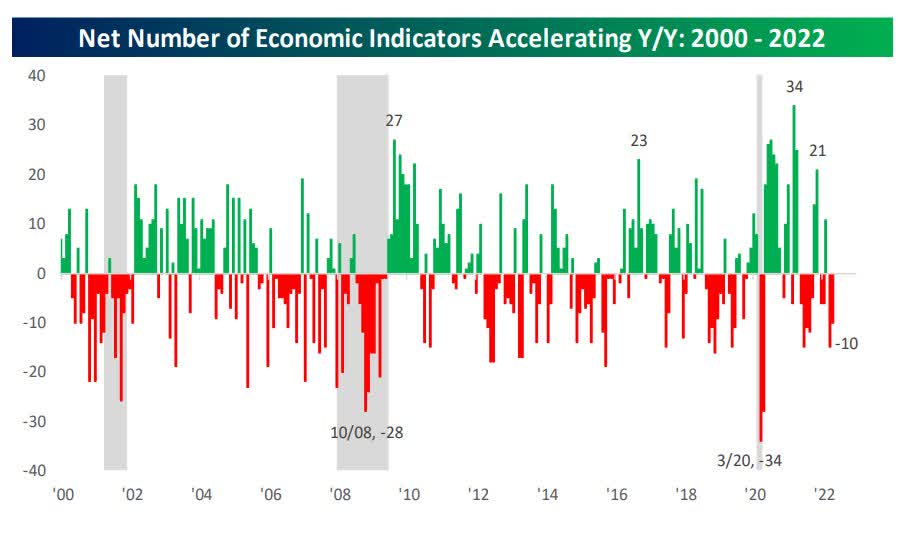

The final a number of weeks of financial information have been disappointing when it comes to financial momentum and exercise relative to expectations. The chart under exhibits the month-to-month internet variety of indicators displaying optimistic momentum of their yr/yr readings going again to 2000.

Bespoke Economic system Index (www.bespokepremium.com)

The present stage of -10 is hardly a historic excessive, nevertheless it’s not optimistic both. Not solely that, however for the final yr, the web variety of indicators exhibiting optimistic momentum has been optimistic simply thrice. The speed of progress has been downshifted.

U.S. leading index dropped 0.4% to 118.3 in Might following April’s 0.4% decline to 118.8. That is the primary back-to-back set of declines since April and March 2020. Of the ten parts that make up the index, 4 made unfavorable contributions, led by inventory costs, client expectations, and constructing permits. Additionally, 5 of the parts made optimistic contributions, led by the rate of interest unfold.

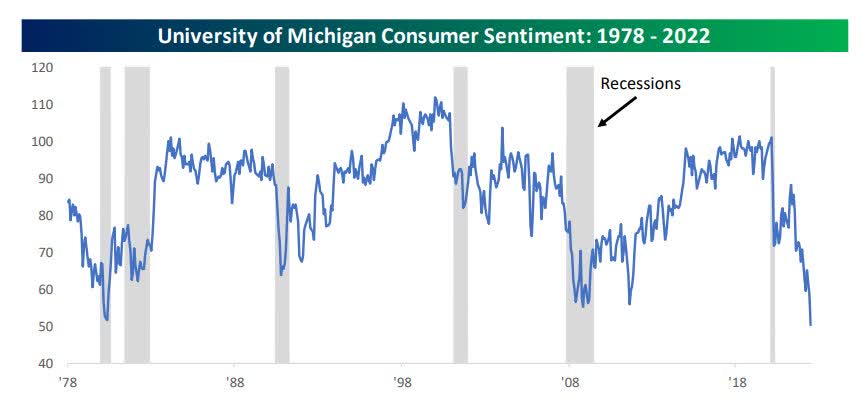

Loads of analysts/economists proceed to debate IF/WHEN a recession will enter the scene. There are all types of knowledge that go into financial forecasts, however typically a easy chart can inform the story fairly properly.

Client sentiment (www.bespokepremium.com)

Based mostly on that ugly image, we may already be in a recession. Q1 was unfavorable and everybody wrote off that report as an outlier. We have seen the Q2 GDP forecast come down from 3% to 2% and now the Atlanta GDPNow model has Q2 coming in at ZERO. I’ve warned that GDP was too excessive since This autumn 2021, once I said there have been NO pro-growth insurance policies in place, I used to be attacked by the BIASED “agenda followers”. Nothing has modified. Economists have both been caught off guard by the velocity of the demise OR they merely have their head within the sand and shopping for into the “rhetoric” out of D.C., and that rhetoric continues to be pervasive now.

Buyers should be aware of the information, keep away from the “noise”, lose their BIAS and depart the GDP dialogue to others.

Inflation

The principle offender for file low sentiment is Inflation. This week’s PPI report included a 1.6% PPI rise that left an increase within the y/y gauge to a 47-year excessive of 16.7% from prior 47-year highs of 15.7% and 15.4%. As we speak’s y/y rise marks the biggest achieve relationship again to an 18.3% enhance in December of 1974 with the primary OPEC oil embargo. The file achieve was a 19.6% y/y climb in November of 1974.

Client

U.S. retail sales declined by 0.9% in Might with ex-auto gross sales rising 0.5%. These comply with respective positive aspects of 0.7% and 0.4% in April. Gross sales excluding autos, fuel, and constructing supplies edged up 0.1% versus the prior 0.9% leap in April and 0.9% achieve in March.

Regardless of the decline on the headline stage, breadth in Might’s report was narrowly optimistic with seven sectors displaying month-over-month progress and 6 had been declining. The most important winner for the month, sadly, was Gasoline Stations, which elevated near 4%. The one different sector that noticed progress of greater than 1% was Meals and Beverage Shops. The truth that these two sectors skilled such robust progress on the expense of most different sectors illustrates the inflationary pressures of upper fuel and meals costs crowding out spending in different areas of the economic system.

On the draw back, Autos noticed the biggest decline in Might with a drop of three.5%, adopted by Electronics & Home equipment at -1.3%. Not solely are these sectors down m/m, however they’re additionally two of solely three sectors the place y/y gross sales are down. The On-line sector was additionally a notable laggard in Might as gross sales fell practically 1% and at the moment are lagging the tempo of total headline Retail Gross sales on a y/y foundation.

Small Enterprise

NFIB Small Business Index was unchanged in April, remaining at 93.2 and the fourth consecutive month under the 48-year common of 98. Small enterprise house owners anticipating higher enterprise situations over the subsequent six months decreased one level to a internet unfavorable 50%, the bottom stage recorded within the 48-year-old survey.

Key findings embody:

- Forty-seven % of homeowners reported job openings that would not be crammed, unchanged from March.

- The online % of homeowners elevating common promoting costs decreased two factors to a internet 70% (seasonally adjusted), two factors under final month’s highest studying.

- The online % of homeowners who count on actual gross sales to be larger elevated six factors from March to a internet unfavorable 12%

Inflation continues to be an issue for small companies with 32% of small enterprise house owners reporting it is their single most vital drawback in working their enterprise, the very best studying for the reason that fourth quarter of 1980.

Manufacturing

The Empire State index bounced to -1.2 adopted by a Might plunge to -11.6 from a 4-month excessive of 24.6 in April. We now have unfavorable headline readings in 4 of the final six months, and they’re the one unfavorable figures since June of 2020.

The Philly Fed drop to a 2-year low of -3.3 in June marked the primary unfavorable studying since Might of 2020, following a Might drop to 2.6 from 17.6 in April and a 4-month excessive of 27.4 in March. The ISM-adjusted Philly Fed additionally plunged to 52.6, which was additionally the bottom studying since Might of 2020.

The 0.2% U.S. industrial production rise in Might after a tiny internet upward revision left a report that tracked estimates, with part swings that additionally largely tracked assumptions.

Housing

NAHB housing market index slid 2 ticks in June to 67 after dropping 8 factors to 69 in Might. It’s a fifth straight month-to-month drop. It was at 81 final June and at an all-time peak of 90 in November 2020. The only-family gross sales index dipped 1 tick to 77 in June after slumping 8 factors to 78 final month. The NAHB famous the housing market faces challenges from each the demand and provide sides amid rising development and supplies prices and growing mortgage charges.

The U.S. housing starts report sharply undershot estimates with a major weak point for begins, permits, and begins beneath development, although completions bounced sharply in Might. Begins plunged 14.4% to a 1.54 million clip in Might. Constructing permits fell 7.0% to a 1.69 million charge. Begins beneath development rose simply 0.4% to 1.66 million to depart the smallest achieve since September of 2020.

Housing completions surged 9.1% to a still-lean 1.46 million charge. Completions are nonetheless monitoring under the trail implied by permits and begins doubtless as a result of materials shortages. Hovering mortgage charges are impacting begins and permits, alongside the massive hit to new and present dwelling gross sales.

Earnings

Inflation is wreaking havoc on shoppers and plenty of members are shifting out of the inventory market suggesting an financial slowdown is right here or coming. In that case, earnings estimates for subsequent yr are too excessive. We have seen reviews and commentary just lately suggesting that the current pullback in shares was making the price-earnings a number of on the S&P 500 very enticing. I’ve advised that it’s completely regular for PE ratios to return down as a result of the expansion section has ended. BUT that does not essentially make them “enticing”.

EPS estimates are doubtless too excessive and I would not try to make use of these earnings forecasts to foretell the ahead PE ratio on the S&P 500. Relatively than attempting to pinpoint a variety, I feel we’d be a lot better off attempting to determine if earnings shall be larger or decrease subsequent yr than they’re this yr. So whereas many pundits put a variety of emphasis on such metrics, the actual query is what sort of PE a number of buyers will place on these earnings.

When buyers are frightened about earnings they have an inclination to position a low a number of on earnings; and, when buyers are ebullient they place a excessive a number of on them. So the funding trick turns into how one can anticipate what buyers are prepared to pay for “ahead” earnings. It is a on condition that we have to begin ratcheting down earnings expectations and what buyers are going to pay for them.

Lastly, utilizing a PE ratio as a “timing ” device has by no means labored.

The Every day Chart of the S&P 500 (SPY)

The waterfall decline has picked up momentum. Just like my OLD maxim of Power begets Power, it’s now Weak point begets extra Weak point.

S&P 500 (www.FreeStockcharts.com)

We frequently see analysts have a tough time selecting a market TOP, the identical is true for attempting to select a BOTTOM. It is a guessing recreation and one which buyers needn’t play. It is also a good suggestion to keep away from pundits that wish to toss round forecasts that exit for months. We will not predict subsequent week but they may inform us what the S&P shall be at year-end. This can be a course of and sooner or later, there shall be sufficient proof to place the items of the puzzle collectively and give you a call.

The waterfall decline paused on Friday. Now it’s a matter of whether or not a rally can take form and transfer the index again to resistance. Sadly, the slope of the pattern strains is suggesting this market weak point is probably not over. Resistance shall be formidable and in the meanwhile, ought to cap any rally try.

Funding Backdrop

At first of buying and selling this week, this was the typical inventory’s drawdown by index:

S&P 500: -28.4%

Russell 3,000: -42.4%

Nasdaq Composite: -50.5%”

Huge Dispersion in Sector Efficiency

We have talked about this since February. Not a lot has labored and the state of affairs acquired worse because the yr unfolded. It has been “Power” and never a lot else. As inflation surges, financial progress slows, the Fed hikes charges, and provide chain issues proceed to plague the economic system. It has been virtually inconceivable to seek out wherever to cover.

Moreover Power, the one different sector up on a YTD foundation was Utilities. (The sub-sector of Commodities (BCI) can also be optimistic in ’22). On the draw back, the worst-performing sector has been Client Discretionary which was down a whopping 26.3%. Together with Client Discretionary, each Communication Providers and Know-how had been additionally down over 20% YTD.

One phrase, BEARISH. There are NO positives that may be gleaned from the quick, intermediate, or long-term tendencies. I am going to let others forecast a backside, I’ve my very own manner of attempting to establish when shares may flip. For now, the consensus forecasts are specializing in the 3200-3500 vary. The PRIMARY pattern is down and each investor that doesn’t have a multi-year time horizon needs to be targeted on preserving capital. These with multi-year time horizons fall into a distinct class and dollar-cost averaging because the market drop has confirmed to be an exquisite technique for many years. Nonetheless, I notice not each investor has that luxurious.

With an excessive oversold situation at hand, I do count on to see a “bounce” within the indices, and maybe the brand new “commerce” shall be cash taken from the Power sector and moved into beaten-down expertise shares.

Thanks for studying this evaluation. Should you loved this text thus far, this subsequent part supplies a fast style of what members of my market service obtain in DAILY updates. Should you discover these weekly articles helpful, you might wish to be a part of a neighborhood of SAVVY Buyers which have found “how the market works”.

The 2022 Playbook is now “Lean and Imply”

Sure, that’s appropriate, alternatives are condensed in Power and Commodities. I’ve dropped Healthcare this week as that sector has now dipped into BEAR market territory as properly. Nonetheless, I nonetheless like choose Pharma firms that pay above-average dividends. The message to purchasers and members of my service has been the identical. Stick with what’s working.

My “canary message” was a warning relating to the Financials, Transports, Semiconductors, and Small Caps. I used them as a “inform” for what route the economic system was headed to assist forge a near-term technique. They despatched their messages for the economic system and since that day the S&P is off 18%. There shall be instances when they seem like revived, however, till there’s a determined swing within the technical image the place rallies take out resistance ranges, they proceed to warn concerning the near-term outlook.

There isn’t a have to get into particulars on the sector exercise this week. All eleven sectors added to their year-to-date losses. Power (XLE) wasn’t resistant to the selloff dropping 17% this week. I’ll proceed to search for assist areas to HOLD in choose vitality names as this dip appears to be like extra like a possibility to reload, relatively than get out.

Inexperienced Power

It’s THE subject, it’s THE theme that drives many individuals as of late. To some, it’s a type of faith the place fossil fuels are the satan and nobody, however NO ONE needs to be related to something to do with oil together with investing. There are pension funds and choose cash managers which have gone the inexperienced route and dissed the extra typical vitality shares. They’ve been destroyed. It’s not solely the truth that their selection in inexperienced investments has gone down a lot, however they’ve additionally missed among the best funding tales that I’ve witnessed in my profession.

Given the runup in vitality costs, you’d suppose that various vitality shares could be ripping larger as shoppers of vitality search for options, however that hasn’t been the case. The photo voltaic trade acquired a lift when the Biden administration introduced plans for a brand new federal program to assist photo voltaic panel manufacturing through the removing of import tariffs. The Invesco Photo voltaic Power ETF (TAN) rallied shortly and traded above its 200-Day shifting common for the primary time since December. Sadly, TAN was unable to remain above its downward sloping 200-DMA reinforcing its downtrend. The LT chart stays in a BEAR market setup.

It was an analogous image for the broader clear vitality area because the iShares World Clear Power ETF (ICLN) was unable to even commerce above its 200-DMA on an intraday foundation. When a inventory or index repeatedly tries and fails to commerce again above a downward sloping key shifting common, it represents traditional bear market conduct, and till these tendencies can reverse themselves, buyers are normally higher served on the sidelines.

There was a time when these shares wildly outperformed the S&P 500 in a low-interest charge backdrop, however with charges anticipated to rise, the headwind of the debt that these firms compile offsets the optimistic tailwind of upper conventional vitality costs.

In distinction, conventional vitality firms are money move machines.

Power

After posting a 60% return within the first 5+ months this yr the Power ETF (XLE) suffered its work week in fairly some time giving again 17% of these positive aspects. It’s the ONE sector that is still in a Longer-term Bullish setting. As soon as the mud settles at assist ranges, shares with 8-10% dividend yields will as soon as once more be offered as bargains.

Worldwide Scene

From a technical perspective, China continues to be a turnaround story. I’ve already famous how their inventory market has outperformed the remainder of the globe just lately. There’s a good motive why that’s the case. Inventory markets don’t care about absolutes, they care about change. It is all about whether or not a market sees a optimistic or a unfavorable change within the MACRO scene. Within the case of the U.S, the change is decidedly unfavorable. The MACRO scene has been upended by Inflation and the opportunity of a recession.

It is simply the alternative in China, positive they’ve their “political” viewpoints which have brought on angst of their markets, however their change is seen as optimistic. Sooner or later, this seemingly infinite collection of lockdowns finish. Inflation will not be rampant and there’s no menace their economic system will tip into recession now.

For positive the united statesis additionally loaded with “political” viewpoints, which have spawned a bevy of “dangers” right here. There isn’t a want to enter particulars on all of them now, they’ve all been documented utilizing info. When now we have an economic system firing on all cylinders immediately on the point of recession, it is obvious these political opinions are on the very least exacerbating the issues. It’s for all of these causes that I conclude that China is definitely worth the danger and it appears prudent to get on board what might be an enormous turnaround story.

Cryptocurrency

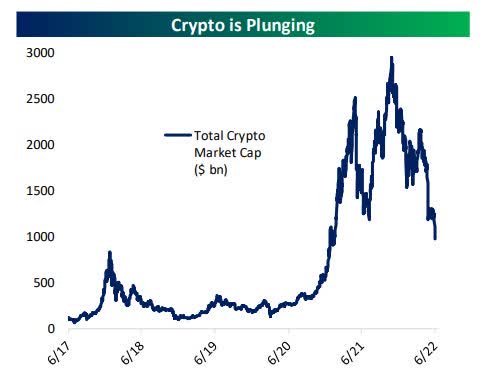

The emergence of crypto markets has been one of the crucial speedy wealth creation occasions in human historical past. From mid-June 2017 by the beginning of November 2021, the overall market cap of the crypto universe rose by 2761%, or $2.845 Trillion. Wealth destruction is proving virtually as speedy on the draw back. Over the previous week, the overall crypto market cap fell over 30% or by $350 Billion and is now again under $1 trillion for the primary time since January thirtieth of 2021.

Bitcoin (www.bespokepremium.com)

That decline added to the weak point that was in place since March. This area is overloaded with leverage and margin calls are doubtless resulting in pressured promoting.

Crypto is neither a retailer of worth nor a hedge in opposition to inflation. It’s a buying and selling automobile and never a lot else. Novice buyers who noticed nothing however upside will now get a lesson in how markets work. The long-term penalties for capital flows to the area of wealth destruction on the dimensions we’re witnessing could take a very long time to play out however they may play out over the approaching years.

Remaining Ideas

What signal are buyers ready for to sign the underside? I preserve listening to the identical commentary again and again the place analysts are questioning IF now we have seen that “capitulation” day.

Granted, we have not but seen the everyday excessive readings within the 10-Day A/D line or the 40+ studying within the VIX that has come to be typical of situations close to market lows. However whereas they look ahead to a bell to be rung, the indicators have been conflicting. There have been numerous 80% and 90% upside quantity days. The month of Might was simply the eleventh month since 1997 that noticed greater than 5 buying and selling days with upside quantity on the NYSE better than 80%. Thus far, it has meant nothing and it demonstrates how tough this market is to navigate.

I’ve addressed this level earlier than so let me repeat. If you’re ready for an all-clear sign, more often than not you aren’t getting it till it is too late. Uncertainty all the time makes its presence felt, particularly on the largest turning factors. In any case, the time period “wall of fear” did not develop into a market maxim for no motive. All we will do is get an in depth lay of the land and take advantage of knowledgeable choices attainable.

Many analysts are utilizing prior charge cycles as their information to forecast a stage the place shares may discover equilibrium. These views are referring to the “typical” Fed mountaineering cycle to put out their technique. The drawback is that this is not your odd charge mountaineering cycle. This one is totally different and it’s EXACTLY what I warned about final yr. While you add unnecessary stimulus to a powerful and rising economic system, you enhance the potential for inflation and that brings the FED into the image WELL BEFORE it was anticipated. They’re right here to battle inflation. They don’t seem to be right here to chill off an overheated economic system. This economic system is weakening, and that is something however a “typical” charge mountaineering cycle.

Maybe the economist and analysts which might be banking on this charge cycle to hint the identical path because the prior cycle shall be appropriate they usually can then proclaim victory when the inventory market finds a backside and stabilizes. The issue is the inventory market NEVER supplies the last word solutions about TOPS or BOTTOMS. The worth motion is main my technique and it is telling a narrative. I want I KNEW how far the indices can fall however I do not, and nobody else does both. Oh however relaxation assured some pundits are predicting something from S&P 2700 to new all-time highs by year-end. Newsflash; they’re GUESSING and I am being variety with that characterization.

In April I despatched a message to purchasers and members of my Savvy Investor Service.

With FEW exceptions this inventory market is uninvestable. Since then the S&P is down 15+%.”

The areas that I believed had been investable are up on common 8-9%. That’s categorized as outperformance. I proceed to take this market state of affairs one transfer at a time. Should you proceed to battle together with your “plan”, my market service is right here to assist. The BEARS stay in management and if anybody doubts that evaluation please return and have a look at the chart of the S&P 500 posted earlier.

Postscript

Please enable me to take a second and remind the entire readers of an vital problem. I present funding recommendation to purchasers and members of my market service. Every week I attempt to offer an funding backdrop that helps buyers make their very own choices. In most of these boards, readers carry a bunch of conditions and variables to the desk when visiting these articles. Subsequently it’s inconceivable to pinpoint what could also be proper for every state of affairs.

In numerous circumstances, I can decide every consumer’s state of affairs/necessities and talk about points with them when wanted. That’s inconceivable with readers of those articles. Subsequently I’ll try to assist kind an opinion with out crossing the road into particular recommendation. Please preserve that in thoughts when forming your funding technique.

THANKS to the entire readers that contribute to this discussion board to make these articles a greater expertise for everybody.

Better of Luck to Everybody!

[ad_2]

Source link