[ad_1]

Should you’re in search of a multi-bagger, there’s a couple of issues to maintain a watch out for. One widespread strategy is to try to discover a firm with returns on capital employed (ROCE) which are growing, along with a rising quantity of capital employed. Should you see this, it sometimes means it is an organization with a fantastic enterprise mannequin and loads of worthwhile reinvestment alternatives. Nevertheless, after investigating Coca-Cola FEMSA. de (NYSE:KOF), we do not assume it is present tendencies match the mould of a multi-bagger.

What’s Return On Capital Employed (ROCE)?

Simply to make clear for those who’re not sure, ROCE is a metric for evaluating how a lot pre-tax revenue (in proportion phrases) an organization earns on the capital invested in its enterprise. The system for this calculation on Coca-Cola FEMSA. de is:

Return on Capital Employed = Earnings Earlier than Curiosity and Tax (EBIT) ÷ (Complete Belongings – Present Liabilities)

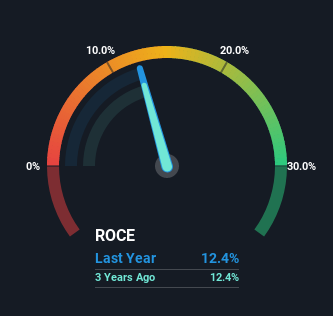

0.12 = Mex$28b ÷ (Mex$284b – Mex$61b) (Primarily based on the trailing twelve months to March 2022).

So, Coca-Cola FEMSA. de has an ROCE of 12%. In absolute phrases, that is a fairly regular return, and it is considerably near the Beverage trade common of 13%.

Check out our latest analysis for Coca-Cola FEMSA. de

Within the above chart we’ve measured Coca-Cola FEMSA. de’s prior ROCE in opposition to its prior efficiency, however the future is arguably extra necessary. Should you’re , you may view the analysts predictions in our free report on analyst forecasts for the company.

So How Is Coca-Cola FEMSA. de’s ROCE Trending?

There hasn’t been a lot to report for Coca-Cola FEMSA. de’s returns and its stage of capital employed as a result of each metrics have been regular for the previous 5 years. This tells us the corporate is not reinvesting in itself, so it is believable that it is previous the expansion part. With that in thoughts, until funding picks up once more sooner or later, we would not count on Coca-Cola FEMSA. de to be a multi-bagger going ahead. That in all probability explains why Coca-Cola FEMSA. de has been paying out 66% of its earnings as dividends to shareholders. These mature companies sometimes have dependable earnings and never many locations to reinvest them, so the subsequent most suitable choice is to place the earnings into shareholders pockets.

In Conclusion…

We will conclude that with regard to Coca-Cola FEMSA. de’s returns on capital employed and the tendencies, there is not a lot change to report on. And within the final 5 years, the inventory has given away 18% so the market does not look too hopeful on these tendencies strengthening any time quickly. On the entire, we aren’t too impressed by the underlying tendencies and we predict there could also be higher probabilities of discovering a multi-bagger elsewhere.

Should you’re nonetheless curious about Coca-Cola FEMSA. de it is value trying out our FREE intrinsic value approximation to see if it is buying and selling at a lovely worth in different respects.

Whereas Coca-Cola FEMSA. de might not presently earn the very best returns, we have compiled a listing of firms that presently earn greater than 25% return on fairness. Try this free list here.

Have suggestions on this text? Involved concerning the content material? Get in touch with us immediately. Alternatively, e mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is normal in nature. We offer commentary based mostly on historic information and analyst forecasts solely utilizing an unbiased methodology and our articles will not be meant to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your aims, or your monetary scenario. We goal to deliver you long-term targeted evaluation pushed by basic information. Notice that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link