[ad_1]

To discover a multi-bagger inventory, what are the underlying developments we should always search for in a enterprise? Amongst different issues, we’ll wish to see two issues; firstly, a rising return on capital employed (ROCE) and secondly, an growth within the firm’s quantity of capital employed. In case you see this, it sometimes means it is an organization with an awesome enterprise mannequin and loads of worthwhile reinvestment alternatives. Talking of which, we observed some nice modifications in Corning’s (NYSE:GLW) returns on capital, so let’s take a look.

Return On Capital Employed (ROCE): What’s it?

Simply to make clear in the event you’re not sure, ROCE is a metric for evaluating how a lot pre-tax revenue (in proportion phrases) an organization earns on the capital invested in its enterprise. Analysts use this system to calculate it for Corning:

Return on Capital Employed = Earnings Earlier than Curiosity and Tax (EBIT) ÷ (Whole Property – Present Liabilities)

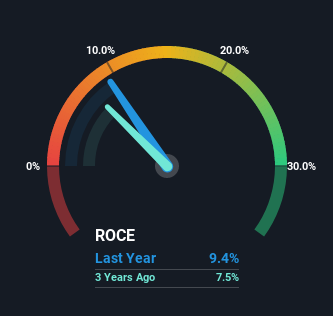

0.094 = US$2.4b ÷ (US$30b – US$5.1b) (Primarily based on the trailing twelve months to March 2022).

So, Corning has an ROCE of 9.4%. In absolute phrases, that is a low return but it surely’s across the Digital business common of 11%.

See our latest analysis for Corning

Above you may see how the present ROCE for Corning compares to its prior returns on capital, however there’s solely a lot you may inform from the previous. In case you’re , you may view the analysts predictions in our free report on analyst forecasts for the company.

What Can We Inform From Corning’s ROCE Development?

Corning is exhibiting promise provided that its ROCE is trending up and to the best. Extra particularly, whereas the corporate has saved capital employed comparatively flat over the past 5 years, the ROCE has climbed 59% in that very same time. So it is doubtless that the enterprise is now reaping the complete advantages of its previous investments, for the reason that capital employed hasn’t modified significantly. It is price trying deeper into this although as a result of whereas it is nice that the enterprise is extra environment friendly, it may also imply that going ahead the areas to speculate internally for the natural development are missing.

Our Take On Corning’s ROCE

To sum it up, Corning is accumulating greater returns from the identical quantity of capital, and that is spectacular. For the reason that inventory has solely returned 20% to shareholders over the past 5 years, the promising fundamentals will not be acknowledged but by traders. So with that in thoughts, we predict the inventory deserves additional analysis.

Another factor, we have noticed 1 warning sign facing Corning that you simply may discover fascinating.

For individuals who wish to spend money on stable firms, try this free list of companies with solid balance sheets and high returns on equity.

Have suggestions on this text? Involved in regards to the content material? Get in touch with us instantly. Alternatively, e mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is basic in nature. We offer commentary primarily based on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles will not be meant to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your targets, or your monetary scenario. We intention to carry you long-term centered evaluation pushed by elementary knowledge. Observe that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link