[ad_1]

To discover a multi-bagger inventory, what are the underlying tendencies we should always search for in a enterprise? Usually, we’ll wish to discover a pattern of rising return on capital employed (ROCE) and alongside that, an increasing base of capital employed. This exhibits us that it is a compounding machine, in a position to regularly reinvest its earnings again into the enterprise and generate increased returns. Having stated that, from a primary look at Zalando (ETR:ZAL) we aren’t leaping out of our chairs at how returns are trending, however let’s have a deeper look.

Understanding Return On Capital Employed (ROCE)

If you have not labored with ROCE earlier than, it measures the ‘return’ (pre-tax revenue) an organization generates from capital employed in its enterprise. Analysts use this components to calculate it for Zalando:

Return on Capital Employed = Earnings Earlier than Curiosity and Tax (EBIT) ÷ (Complete Property – Present Liabilities)

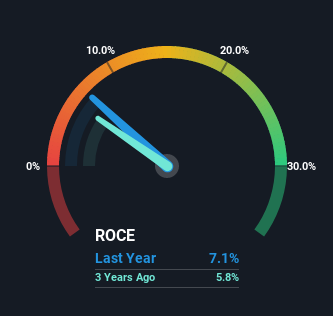

0.071 = €265m ÷ (€6.8b – €3.1b) (Primarily based on the trailing twelve months to March 2022).

So, Zalando has an ROCE of seven.1%. By itself that is a low return, however in comparison with the common of 5.4% generated by the On-line Retail trade, it is a lot better.

View our latest analysis for Zalando

Within the above chart now we have measured Zalando’s prior ROCE towards its prior efficiency, however the future is arguably extra necessary. If you would like, you’ll be able to take a look at the forecasts from the analysts protecting Zalando here for free.

The Development Of ROCE

Once we appeared on the ROCE pattern at Zalando, we did not acquire a lot confidence. To be extra particular, ROCE has fallen from 13% during the last 5 years. Though, given each income and the quantity of property employed within the enterprise have elevated, it may recommend the corporate is investing in progress, and the additional capital has led to a short-term discount in ROCE. And if the elevated capital generates extra returns, the enterprise, and thus shareholders, will profit in the long term.

One other factor to notice, Zalando has a excessive ratio of present liabilities to complete property of 45%. This successfully implies that suppliers (or short-term collectors) are funding a big portion of the enterprise, so simply bear in mind that this could introduce some components of threat. Whereas it is not essentially a nasty factor, it may be helpful if this ratio is decrease.

The Backside Line

Whereas returns have fallen for Zalando in latest occasions, we’re inspired to see that gross sales are rising and that the enterprise is reinvesting in its operations. And there could possibly be a chance right here if different metrics look good too, as a result of the inventory has declined 35% within the final 5 years. So we predict it would be worthwhile to look additional into this inventory given the tendencies look encouraging.

One remaining observe, it’s best to study concerning the 3 warning signs we’ve spotted with Zalando (including 1 which doesn’t sit too well with us) .

Whereas Zalando could not presently earn the very best returns, we have compiled an inventory of corporations that presently earn greater than 25% return on fairness. Try this free list here.

Have suggestions on this text? Involved concerning the content material? Get in touch with us straight. Alternatively, electronic mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is normal in nature. We offer commentary based mostly on historic information and analyst forecasts solely utilizing an unbiased methodology and our articles will not be meant to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary state of affairs. We goal to convey you long-term targeted evaluation pushed by basic information. Word that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link