[ad_1]

If we need to discover a potential multi-bagger, usually there are underlying tendencies that may present clues. Firstly, we’ll need to see a confirmed return on capital employed (ROCE) that’s growing, and secondly, an increasing base of capital employed. Put merely, a lot of these companies are compounding machines, which means they’re frequently reinvesting their earnings at ever-higher charges of return. That is why once we briefly checked out Ringmetall’s (ETR:HP3A) ROCE pattern, we had been very proud of what we noticed.

What’s Return On Capital Employed (ROCE)?

If you have not labored with ROCE earlier than, it measures the ‘return’ (pre-tax revenue) an organization generates from capital employed in its enterprise. The components for this calculation on Ringmetall is:

Return on Capital Employed = Earnings Earlier than Curiosity and Tax (EBIT) ÷ (Whole Property – Present Liabilities)

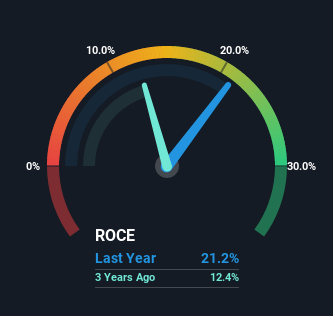

0.21 = €19m ÷ (€124m – €33m) (Based mostly on the trailing twelve months to December 2021).

Due to this fact, Ringmetall has an ROCE of 21%. In absolute phrases that is a fantastic return and it is even higher than the Equipment business common of 8.6%.

Check out our latest analysis for Ringmetall

Above you’ll be able to see how the present ROCE for Ringmetall compares to its prior returns on capital, however there’s solely a lot you’ll be able to inform from the previous. If you would like, you’ll be able to try the forecasts from the analysts protecting Ringmetall here for free.

How Are Returns Trending?

By way of Ringmetall’s historical past of ROCE, it is fairly spectacular. Over the previous 5 years, ROCE has remained comparatively flat at round 21% and the enterprise has deployed 105% extra capital into its operations. Returns like this are the envy of most companies and given it has repeatedly reinvested at these charges, that is even higher. If these tendencies can proceed, it would not shock us if the corporate grew to become a multi-bagger.

Our Take On Ringmetall’s ROCE

In the long run, the corporate has confirmed it may possibly reinvest it is capital at excessive charges of returns, which you will bear in mind is a trait of a multi-bagger. And the inventory has adopted swimsuit returning a significant 79% to shareholders during the last 5 years. So whereas traders appear to be recognizing these promising tendencies, we nonetheless imagine the inventory deserves additional analysis.

Ringmetall does have some dangers, we seen 2 warning signs (and 1 which is concerning) we expect you need to learn about.

If you wish to seek for extra shares which have been incomes excessive returns, try this free list of stocks with solid balance sheets that are also earning high returns on equity.

Have suggestions on this text? Involved concerning the content material? Get in touch with us straight. Alternatively, electronic mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is normal in nature. We offer commentary based mostly on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles are usually not meant to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your aims, or your monetary state of affairs. We intention to deliver you long-term targeted evaluation pushed by elementary knowledge. Observe that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link