[ad_1]

Discovering a enterprise that has the potential to develop considerably just isn’t simple, however it’s potential if we have a look at a couple of key monetary metrics. Firstly, we’ll need to see a confirmed return on capital employed (ROCE) that’s growing, and secondly, an increasing base of capital employed. Put merely, most of these companies are compounding machines, that means they’re frequently reinvesting their earnings at ever-higher charges of return. Nevertheless, after investigating Fortis (TSE:FTS), we do not assume it is present traits match the mildew of a multi-bagger.

Understanding Return On Capital Employed (ROCE)

For those who aren’t certain what ROCE is, it measures the quantity of pre-tax income an organization can generate from the capital employed in its enterprise. Analysts use this components to calculate it for Fortis:

Return on Capital Employed = Earnings Earlier than Curiosity and Tax (EBIT) ÷ (Complete Belongings – Present Liabilities)

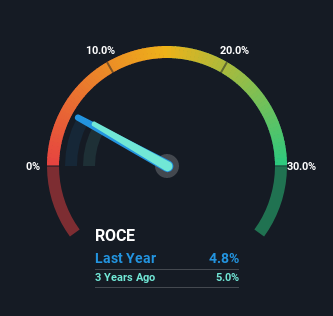

0.048 = CA$2.5b ÷ (CA$58b – CA$4.9b) (Based mostly on the trailing twelve months to March 2022).

Thus, Fortis has an ROCE of 4.8%. By itself that is a low return on capital but it surely’s consistent with the business’s common returns of 4.8%.

See our latest analysis for Fortis

Within the above chart we’ve got measured Fortis’ prior ROCE in opposition to its prior efficiency, however the future is arguably extra vital. In case you’re , you’ll be able to view the analysts predictions in our free report on analyst forecasts for the company.

So How Is Fortis’ ROCE Trending?

By way of Fortis’ historic ROCE development, it would not precisely demand consideration. The corporate has employed 22% extra capital within the final 5 years, and the returns on that capital have remained secure at 4.8%. This poor ROCE would not encourage confidence proper now, and with the rise in capital employed, it is evident that the enterprise is not deploying the funds into excessive return investments.

Our Take On Fortis’ ROCE

In conclusion, Fortis has been investing extra capital into the enterprise, however returns on that capital have not elevated. Because the inventory has gained a powerful 55% over the past 5 years, buyers should assume there’s higher issues to come back. Finally, if the underlying traits persist, we would not maintain our breath on it being a multi-bagger going ahead.

If you wish to know among the dangers going through Fortis we have discovered 2 warning signs (1 is regarding!) that try to be conscious of earlier than investing right here.

Whereas Fortis could not at the moment earn the very best returns, we have compiled a listing of corporations that at the moment earn greater than 25% return on fairness. Try this free list here.

Have suggestions on this text? Involved concerning the content material? Get in touch with us straight. Alternatively, e mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is normal in nature. We offer commentary primarily based on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles aren’t supposed to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary state of affairs. We purpose to convey you long-term centered evaluation pushed by basic knowledge. Notice that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link