[ad_1]

David Iben put it nicely when he stated, ‘Volatility will not be a danger we care about. What we care about is avoiding the everlasting lack of capital.’ After we take into consideration how dangerous an organization is, we at all times like to take a look at its use of debt, since debt overload can result in smash. As with many different corporations NTPC Restricted (NSE:NTPC) makes use of debt. However is that this debt a priority to shareholders?

What Threat Does Debt Convey?

Typically talking, debt solely turns into an actual drawback when an organization cannot simply pay it off, both by elevating capital or with its personal money stream. In the end, if the corporate cannot fulfill its authorized obligations to repay debt, shareholders might stroll away with nothing. Nonetheless, a extra frequent (however nonetheless pricey) incidence is the place an organization should concern shares at bargain-basement costs, completely diluting shareholders, simply to shore up its steadiness sheet. Having stated that, the most typical scenario is the place an organization manages its debt moderately nicely – and to its personal benefit. After we take into consideration an organization’s use of debt, we first take a look at money and debt collectively.

Check out our latest analysis for NTPC

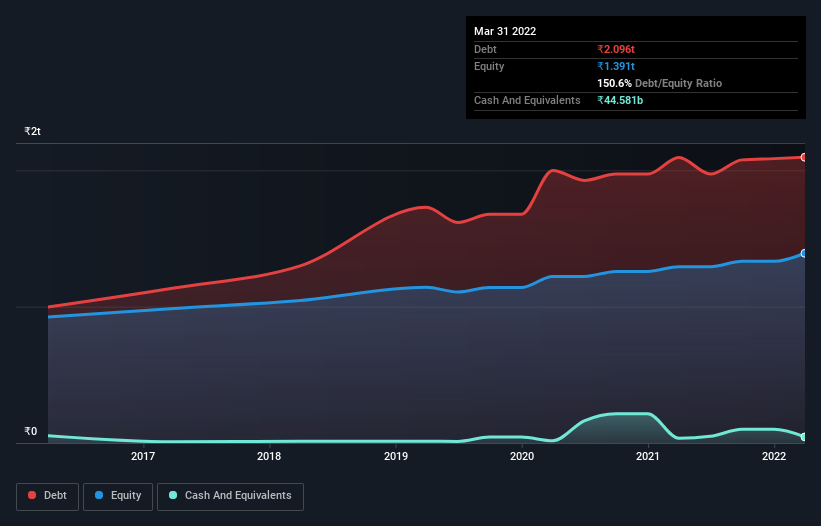

What Is NTPC’s Web Debt?

As you possibly can see under, NTPC had ₹2.10t of debt, at March 2022, which is about the identical because the 12 months earlier than. You may click on the chart for better element. Nonetheless, it does have ₹44.6b in money offsetting this, resulting in web debt of about ₹2.05t.

How Wholesome Is NTPC’s Stability Sheet?

Zooming in on the newest steadiness sheet information, we will see that NTPC had liabilities of ₹765.9b due inside 12 months and liabilities of ₹2.01t due past that. Offsetting these obligations, it had money of ₹44.6b in addition to receivables valued at ₹276.8b due inside 12 months. So its liabilities outweigh the sum of its money and (near-term) receivables by ₹2.45t.

This deficit casts a shadow over the ₹1.44t firm, like a colossus towering over mere mortals. So we might watch its steadiness sheet intently, definitely. In spite of everything, NTPC would possible require a serious re-capitalisation if it needed to pay its collectors as we speak.

We use two important ratios to tell us about debt ranges relative to earnings. The primary is web debt divided by earnings earlier than curiosity, tax, depreciation, and amortization (EBITDA), whereas the second is what number of occasions its earnings earlier than curiosity and tax (EBIT) covers its curiosity expense (or its curiosity cowl, for brief). Thus we contemplate debt relative to earnings each with and with out depreciation and amortization bills.

NTPC has a quite excessive debt to EBITDA ratio of 5.1 which suggests a significant debt load. Nonetheless, its curiosity protection of two.8 is fairly robust, which is an efficient signal. On a lighter observe, we observe that NTPC grew its EBIT by 22% within the final 12 months. If sustained, this development ought to make that debt evaporate like a scarce ingesting water throughout an unnaturally scorching summer season. There isn’t any doubt that we study most about debt from the steadiness sheet. However it’s future earnings, greater than something, that can decide NTPC’s potential to take care of a wholesome steadiness sheet going ahead. So should you’re targeted on the long run you possibly can take a look at this free report showing analyst profit forecasts.

Lastly, a enterprise wants free money stream to repay debt; accounting earnings simply do not minimize it. So it is value checking how a lot of that EBIT is backed by free money stream. Within the final three years, NTPC’s free money stream amounted to 45% of its EBIT, lower than we might count on. That weak money conversion makes it tougher to deal with indebtedness.

Our View

To be frank each NTPC’s web debt to EBITDA and its monitor document of staying on high of its whole liabilities make us quite uncomfortable with its debt ranges. However on the intense facet, its EBIT development charge is an efficient signal, and makes us extra optimistic. Wanting on the larger image, it appears clear to us that NTPC’s use of debt is creating dangers for the corporate. If all goes nicely, that ought to enhance returns, however on the flip facet, the chance of everlasting capital loss is elevated by the debt. When analysing debt ranges, the steadiness sheet is the plain place to begin. However in the end, each firm can include dangers that exist exterior of the steadiness sheet. These dangers will be exhausting to identify. Each firm has them, and we have noticed 2 warning signs for NTPC (of which 1 is regarding!) you must find out about.

If, in any case that, you are extra excited by a quick rising firm with a rock-solid steadiness sheet, then take a look at our list of net cash growth stocks directly.

Have suggestions on this text? Involved in regards to the content material? Get in touch with us instantly. Alternatively, e mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is normal in nature. We offer commentary based mostly on historic information and analyst forecasts solely utilizing an unbiased methodology and our articles should not supposed to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary scenario. We goal to deliver you long-term targeted evaluation pushed by basic information. Be aware that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link