[ad_1]

For rookies, it will possibly appear to be a good suggestion (and an thrilling prospect) to purchase an organization that tells an excellent story to buyers, even when it utterly lacks a observe report of income and revenue. Sadly, excessive danger investments usually have little chance of ever paying off, and plenty of buyers pay a value to be taught their lesson.

In distinction to all that, I choose to spend time on corporations like e.l.f. Magnificence (NYSE:ELF), which has not solely revenues, but additionally income. Now, I am not saying that the inventory is essentially undervalued at present; however I am unable to shake an appreciation for the profitability of the enterprise itself. Conversely, a loss-making firm is but to show itself with revenue, and ultimately the candy milk of exterior capital might run bitter.

Check out our latest analysis for e.l.f. Beauty

How Quick Is e.l.f. Magnificence Rising Its Earnings Per Share?

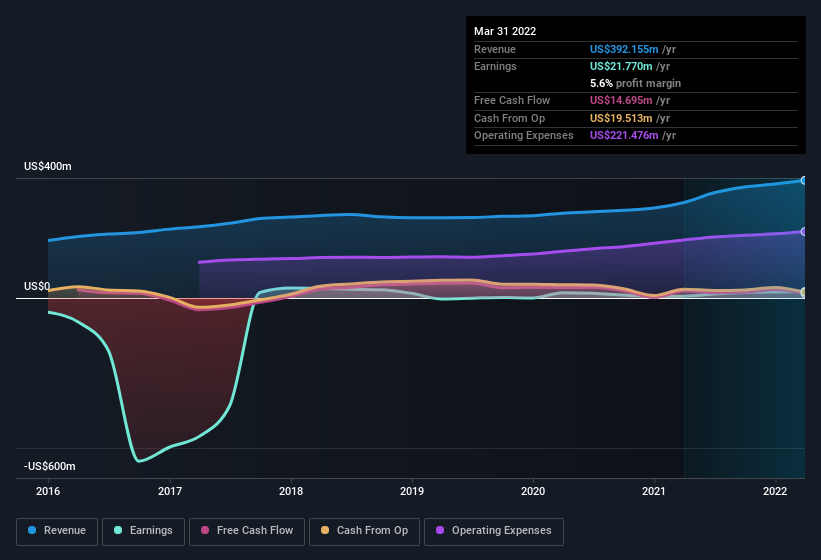

In enterprise, although not in life, income are a key measure of success; and share costs are inclined to replicate earnings per share (EPS). So just like the trace of a smile on a face that I like, rising EPS usually makes me look twice. You possibly can think about, then, that it virtually knocked my socks off once I realized that e.l.f. Magnificence grew its EPS from US$0.13 to US$0.42, in a single quick yr. Regardless that that progress fee is unlikely to be repeated, that appears like a breakout enchancment. However the hot button is discerning whether or not one thing profound has modified, or if it is a only a one-off increase.

I wish to see top-line progress as a sign that progress is sustainable, and I search for a excessive earnings earlier than curiosity and taxation (EBIT) margin to level to a aggressive moat (although some corporations with low margins even have moats). The excellent news is that e.l.f. Magnificence is rising revenues, and EBIT margins improved by 3.8 share factors to 7.6%, over the past yr. Ticking these two containers is an efficient signal of progress, in my e book.

The chart under exhibits how the corporate’s backside and prime traces have progressed over time. For finer element, click on on the picture.

After all the knack is to search out shares which have their finest days sooner or later, not prior to now. You can base your opinion on previous efficiency, in fact, however you might also need to check this interactive graph of professional analyst EPS forecasts for e.l.f. Beauty.

Are e.l.f. Magnificence Insiders Aligned With All Shareholders?

I like firm leaders to have some pores and skin within the sport, so to talk, as a result of it will increase alignment of incentives between the folks working the enterprise, and its true house owners. Consequently, I am inspired by the truth that insiders personal e.l.f. Magnificence shares value a substantial sum. Given insiders personal a small fortune of shares, presently valued at US$74m, they’ve loads of motivation to push the enterprise to succeed. This could maintain them targeted on creating long run worth for shareholders.

Does e.l.f. Magnificence Deserve A Spot On Your Watchlist?

e.l.f. Magnificence’s earnings per share have taken off like a rocket aimed proper on the moon. That EPS progress actually has my consideration, and the massive insider possession solely serves to additional stoke my curiosity. The hope is, in fact, that the robust progress marks a basic enchancment within the enterprise economics. So sure, on this quick evaluation I do assume it is value contemplating e.l.f. Magnificence for a spot in your watchlist. It’s value noting although that now we have discovered 1 warning sign for e.l.f. Beauty that it is advisable take into accounts.

You possibly can spend money on any firm you need. However in case you choose to deal with shares which have demonstrated insider shopping for, right here is a list of companies with insider buying in the last three months.

Please be aware the insider transactions mentioned on this article consult with reportable transactions within the related jurisdiction.

Have suggestions on this text? Involved in regards to the content material? Get in touch with us straight. Alternatively, electronic mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is common in nature. We offer commentary based mostly on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles usually are not supposed to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your aims, or your monetary state of affairs. We intention to convey you long-term targeted evaluation pushed by basic knowledge. Word that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link