[ad_1]

In case you’re undecided the place to begin when searching for the subsequent multi-bagger, there are a number of key developments it’s best to maintain an eye fixed out for. Sometimes, we’ll need to discover a pattern of rising return on capital employed (ROCE) and alongside that, an increasing base of capital employed. In case you see this, it sometimes means it is an organization with an excellent enterprise mannequin and loads of worthwhile reinvestment alternatives. So on that notice, Orissa Minerals Growth (NSE:ORISSAMINE) appears fairly promising with regard to its developments of return on capital.

What’s Return On Capital Employed (ROCE)?

For individuals who do not know, ROCE is a measure of an organization’s yearly pre-tax revenue (its return), relative to the capital employed within the enterprise. Analysts use this method to calculate it for Orissa Minerals Growth:

Return on Capital Employed = Earnings Earlier than Curiosity and Tax (EBIT) ÷ (Whole Property – Present Liabilities)

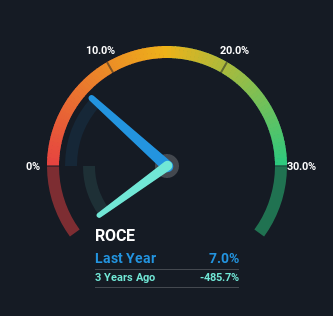

0.07 = ₹95m ÷ (₹4.7b – ₹3.3b) (Primarily based on the trailing twelve months to March 2022).

Subsequently, Orissa Minerals Growth has an ROCE of seven.0%. In absolute phrases, that is a low return and it additionally under-performs the Metals and Mining business common of 17%.

View our latest analysis for Orissa Minerals Development

Whereas the previous isn’t consultant of the longer term, it may be useful to know the way an organization has carried out traditionally, which is why now we have this chart above. In case you’re fascinated by investigating Orissa Minerals Growth’s previous additional, try this free graph of past earnings, revenue and cash flow.

So How Is Orissa Minerals Growth’s ROCE Trending?

It is nice to see that Orissa Minerals Growth has began to generate some pre-tax earnings from prior investments. Traditionally the corporate was producing losses however as we are able to see from the most recent figures referenced above, they’re now incomes 7.0% on their capital employed. Moreover, the enterprise is using 84% much less capital than it was 5 years in the past, and brought at face worth, that may imply the corporate wants much less funds at work to get a return. This might doubtlessly imply that the corporate is promoting a few of its property.

For the report although, there was a noticeable enhance within the firm’s present liabilities over the interval, so we might attribute a few of the ROCE progress to that. The present liabilities has elevated to 71% of complete property, so the enterprise is now extra funded by the likes of its suppliers or short-term collectors. And with present liabilities at these ranges, that is fairly excessive.

In Conclusion…

In the long run, Orissa Minerals Growth has confirmed it is capital allocation abilities are good with these greater returns from much less quantity of capital. For the reason that inventory has solely returned 26% to shareholders over the past 5 years, the promising fundamentals is probably not acknowledged but by buyers. On condition that, we would look additional into this inventory in case it has extra traits that might make it multiply in the long run.

On a separate notice, we have discovered 1 warning sign for Orissa Minerals Development you will most likely need to learn about.

For individuals who prefer to put money into strong corporations, try this free list of companies with solid balance sheets and high returns on equity.

Have suggestions on this text? Involved concerning the content material? Get in touch with us straight. Alternatively, electronic mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is basic in nature. We offer commentary based mostly on historic information and analyst forecasts solely utilizing an unbiased methodology and our articles should not supposed to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary scenario. We goal to deliver you long-term centered evaluation pushed by elementary information. Word that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link