[ad_1]

Should you’re undecided the place to start out when on the lookout for the following multi-bagger, there are a number of key traits you need to hold an eye fixed out for. Firstly, we might wish to determine a rising return on capital employed (ROCE) after which alongside that, an ever-increasing base of capital employed. Should you see this, it usually means it is an organization with an incredible enterprise mannequin and loads of worthwhile reinvestment alternatives. With that in thoughts, the ROCE of Polycab India (NSE:POLYCAB) seems enticing proper now, so lets see what the development of returns can inform us.

Return On Capital Employed (ROCE): What Is It?

For people who aren’t positive what ROCE is, it measures the quantity of pre-tax income an organization can generate from the capital employed in its enterprise. The method for this calculation on Polycab India is:

Return on Capital Employed = Earnings Earlier than Curiosity and Tax (EBIT) ÷ (Complete Belongings – Present Liabilities)

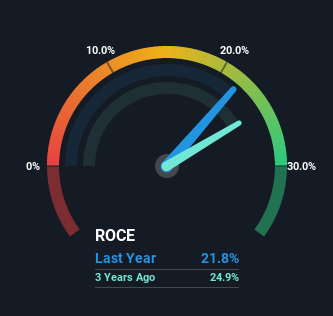

0.22 = ₹12b ÷ (₹70b – ₹14b) (Based mostly on the trailing twelve months to June 2022).

Thus, Polycab India has an ROCE of twenty-two%. In absolute phrases that is an incredible return and it is even higher than the Electrical business common of 13%.

See our latest analysis for Polycab India

Within the above chart we’ve measured Polycab India’s prior ROCE towards its prior efficiency, however the future is arguably extra vital. Should you’re , you possibly can view the analysts predictions in our free report on analyst forecasts for the company.

So How Is Polycab India’s ROCE Trending?

We would be fairly pleased with returns on capital like Polycab India. The corporate has employed 143% extra capital within the final 5 years, and the returns on that capital have remained steady at 22%. With returns that top, it is nice that the enterprise can frequently reinvest its cash at such interesting charges of return. If Polycab India can hold this up, we might be very optimistic about its future.

On a aspect observe, Polycab India has achieved properly to scale back present liabilities to 19% of whole belongings over the past 5 years. This may remove among the dangers inherent within the operations as a result of the enterprise has much less excellent obligations to their suppliers and or short-term collectors than they did beforehand.

In Conclusion…

In abstract, we’re delighted to see that Polycab India has been compounding returns by reinvesting at persistently excessive charges of return, as these are frequent traits of a multi-bagger. And long run traders can be thrilled with the 333% return they’ve obtained over the past three years. So whereas the optimistic underlying traits could also be accounted for by traders, we nonetheless assume this inventory is price wanting into additional.

On a closing observe, we discovered 2 warning signs for Polycab India (1 is concerning) you ought to be conscious of.

Excessive returns are a key ingredient to sturdy efficiency, so take a look at our free listing ofstocks earning high returns on equity with solid balance sheets.

Have suggestions on this text? Involved concerning the content material? Get in touch with us straight. Alternatively, electronic mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is common in nature. We offer commentary based mostly on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles aren’t supposed to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your aims, or your monetary state of affairs. We intention to deliver you long-term targeted evaluation pushed by elementary knowledge. Notice that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link