[ad_1]

To discover a multi-bagger inventory, what are the underlying tendencies we should always search for in a enterprise? In an ideal world, we might wish to see an organization investing extra capital into its enterprise and ideally the returns earned from that capital are additionally growing. Should you see this, it sometimes means it is an organization with an ideal enterprise mannequin and loads of worthwhile reinvestment alternatives. Nevertheless, after investigating Carel Industries (BIT:CRL), we do not suppose it is present tendencies match the mould of a multi-bagger.

Return On Capital Employed (ROCE): What’s it?

For many who do not know, ROCE is a measure of an organization’s yearly pre-tax revenue (its return), relative to the capital employed within the enterprise. Analysts use this formulation to calculate it for Carel Industries:

Return on Capital Employed = Earnings Earlier than Curiosity and Tax (EBIT) ÷ (Complete Belongings – Present Liabilities)

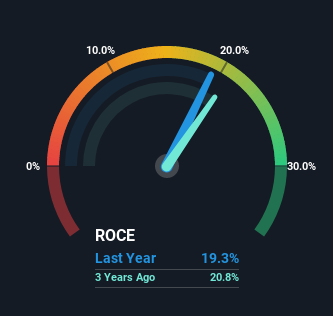

0.19 = €69m ÷ (€519m – €163m) (Based mostly on the trailing twelve months to March 2022).

So, Carel Industries has an ROCE of 19%. By itself, that is an ordinary return, nonetheless it is significantly better than the 7.4% generated by the Constructing business.

Check out our latest analysis for Carel Industries

Within the above chart we have now measured Carel Industries’ prior ROCE towards its prior efficiency, however the future is arguably extra necessary. If you would like, you may try the forecasts from the analysts masking Carel Industries here for free.

So How Is Carel Industries’ ROCE Trending?

On the floor, the development of ROCE at Carel Industries does not encourage confidence. Round 5 years in the past the returns on capital had been 27%, however since then they’ve fallen to 19%. Nevertheless, given capital employed and income have each elevated it seems that the enterprise is presently pursuing progress, on the consequence of quick time period returns. If these investments show profitable, this will bode very effectively for long run inventory efficiency.

The Key Takeaway

In abstract, regardless of decrease returns within the quick time period, we’re inspired to see that Carel Industries is reinvesting for progress and has greater gross sales consequently. And the inventory has adopted swimsuit returning a significant 70% to shareholders during the last three years. So ought to these progress tendencies proceed, we might be optimistic on the inventory going ahead.

Carel Industries does have some dangers although, and we have noticed 1 warning sign for Carel Industries that you simply is likely to be concerned about.

Whereas Carel Industries is not incomes the very best return, try this free list of companies that are earning high returns on equity with solid balance sheets.

Have suggestions on this text? Involved concerning the content material? Get in touch with us immediately. Alternatively, e-mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is normal in nature. We offer commentary based mostly on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles aren’t meant to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your targets, or your monetary scenario. We goal to convey you long-term targeted evaluation pushed by basic knowledge. Observe that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link