[ad_1]

Discovering a enterprise that has the potential to develop considerably is just not straightforward, however it’s potential if we have a look at a number of key monetary metrics. One widespread method is to try to discover a firm with returns on capital employed (ROCE) which might be growing, at the side of a rising quantity of capital employed. Put merely, a lot of these companies are compounding machines, that means they’re regularly reinvesting their earnings at ever-higher charges of return. Having mentioned that, from a primary look at Mainova (FRA:MNV6) we aren’t leaping out of our chairs at how returns are trending, however let’s have a deeper look.

What’s Return On Capital Employed (ROCE)?

If you have not labored with ROCE earlier than, it measures the ‘return’ (pre-tax revenue) an organization generates from capital employed in its enterprise. The method for this calculation on Mainova is:

Return on Capital Employed = Earnings Earlier than Curiosity and Tax (EBIT) ÷ (Whole Belongings – Present Liabilities)

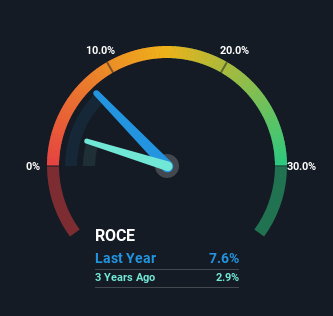

0.076 = €399m ÷ (€6.4b – €1.1b) (Primarily based on the trailing twelve months to December 2021).

Due to this fact, Mainova has an ROCE of seven.6%. In absolute phrases, that is a low return, however it’s a lot better than the Built-in Utilities trade common of 5.2%.

View our latest analysis for Mainova

Whereas the previous is just not consultant of the longer term, it may be useful to know the way an organization has carried out traditionally, which is why we now have this chart above. Should you’re desirous about investigating Mainova’s previous additional, try this free graph of past earnings, revenue and cash flow.

How Are Returns Trending?

By way of Mainova’s historic ROCE pattern, it would not precisely demand consideration. The corporate has persistently earned 7.6% for the final 5 years, and the capital employed inside the enterprise has risen 144% in that point. Given the corporate has elevated the quantity of capital employed, it seems the investments which have been made merely do not present a excessive return on capital.

In Conclusion…

In conclusion, Mainova has been investing extra capital into the enterprise, however returns on that capital have not elevated. For the reason that inventory has gained a formidable 72% during the last 5 years, buyers should suppose there’s higher issues to return. Finally, if the underlying developments persist, we would not maintain our breath on it being a multi-bagger going ahead.

On a separate word, we have discovered 1 warning sign for Mainova you will in all probability need to learn about.

For many who wish to put money into stable firms, try this free list of companies with solid balance sheets and high returns on equity.

Have suggestions on this text? Involved in regards to the content material? Get in touch with us instantly. Alternatively, electronic mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is normal in nature. We offer commentary based mostly on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles should not supposed to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your aims, or your monetary scenario. We intention to convey you long-term targeted evaluation pushed by elementary knowledge. Observe that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link