[ad_1]

Dony/iStock through Getty Pictures

Intro

Shares of Franklin Sources, Inc. (NYSE:BEN) at their current share value of simply over $23 a share now discover themselves down roughly 30% in worth yr thus far. The collapse in a method is shocking given that Franklin Sources (together with its current second-quarter numbers) has now strung collectively 5 consecutive quarters of straight earnings beats. GAAP earnings of $0.68 within the firm‘s current second quarter beat the consensus estimate by $0.05 whereas the corporate‘s gross sales as soon as extra beat projections by a small margin.

In saying the above, consensus earnings revisions for upcoming quarters proceed to get dialed down and that is worrying buyers. On the finish of January this yr, for instance, consensus was estimating that Franklin Sources would report roughly $0.92 per share for its fiscal third quarter. This quantity has already been dialed again to $0.83 per share and we, sadly, see an analogous development for the quarters to comply with.

Latest volatility in fairness markets and the Fed‘s accelerated tightening schedule may very well be construed as being momentary headwinds for Franklin Sources. Assets beneath administration for instance lose a few of their worth in a downturn and Could witnessed a slight drop in belongings beneath administration within the firm‘s fixed-income enterprise in addition to its general fairness section. Nevertheless, hasn‘t Franklin Sources seen this all earlier than? Is not going to the corporate‘s much-improved specialization and experience allow the agency not solely to outlive by elevated volatility but additionally thrive?

Moreover, Franklin Sources‘ improved capabilities with respect to its merchandise stay a piece in movement. We state this as a result of, regardless of the big “Lexington Partners” acquisition which passed off final April, Franklin Sources nonetheless has a battle chest of just about $7 billion in money & investments at its disposal.

This provides us confidence that the corporate has the wherewithal to pivot regarding upcoming investments if certainly the trade warrants such a transfer. Suffice it to say, based mostly on the steep pullback within the share value of BEN, we stay very considering BEN from the lengthy facet and would commerce the inventory within the following format.

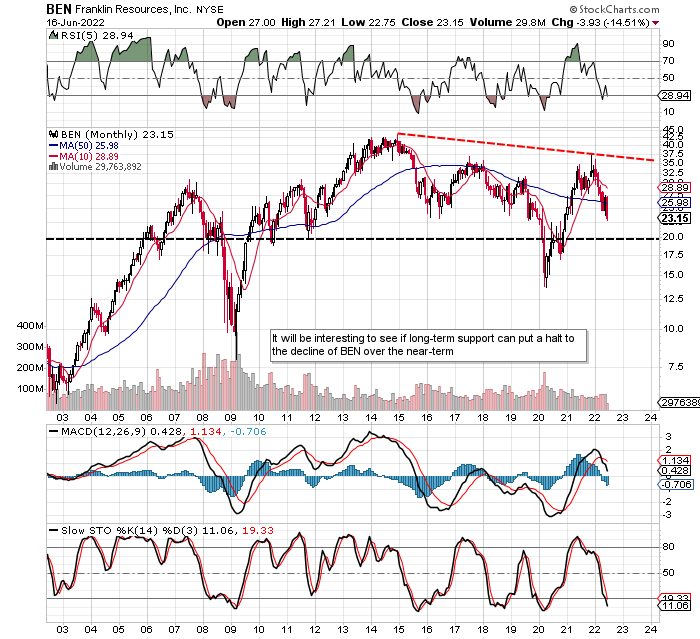

BEN Technical Lengthy-Time period Chart (Stockcharts.com)

Promote Close to-Dated Put Choices

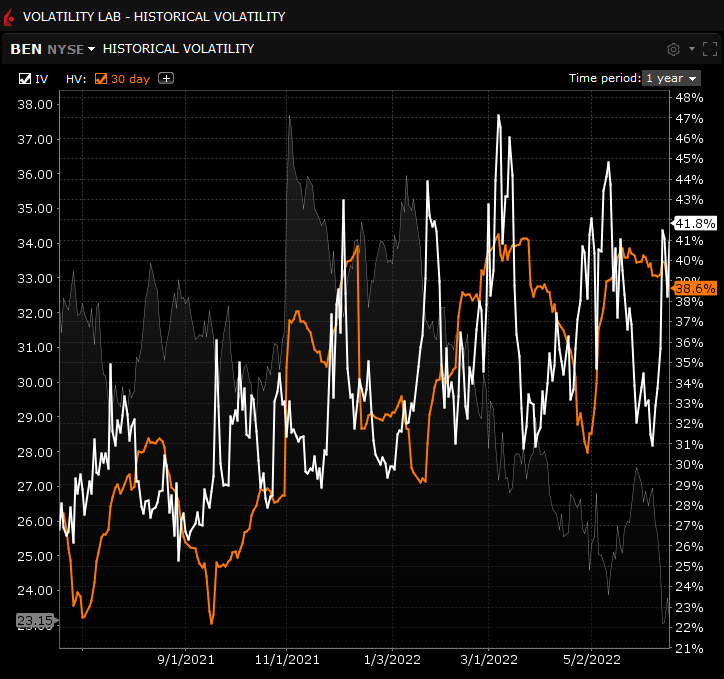

Many occasions when researching particular person shares, buyers get too caught up in interested by the near-term course of their performs and ignore the opposite profit-making prospects. As we are able to see beneath within the implied volatility chart of BEN, IV has now surpassed 40% within the again month and is buying and selling above the inventory‘s historic volatility. This implies present choices costs are inflated which suggests we are able to gather above-average premiums for instance when promoting near-dated put choices. The common July out-of-the-money $22.50 put choices for instance are buying and selling for near $1 per contract which suggests the breakeven for this place can be $21.50 per put choice (100 shares of inventory). To attenuate shopping for energy, our technique can be to roll these choices out in time when examined (and preferable down) which might additionally scale back our breakeven within the place. Let‘s say although after a number of months of rolling, we get assigned inventory or can‘t roll near-term for a credit score which suggests we find yourself holding a basket of shares of BEN with a price foundation of a hypothetical $20 per share. The query then turns into, why would we be completely happy proudly owning shares at this value level?

BEN – Implied Volatility Chart (Interactive Brokers)

Finally, Get “PUT” Lengthy Inventory

BEN‘s valuation (GAAP earnings a number of of 6.22) is clearly low-cost and can be an much more engaging proposition if shares really went considerably decrease. We state this as a result of Franklin is healthily worthwhile as we are able to see from the free money circulation it’s producing ($869 million over the previous 4 quarters). Followers of our work might be conscious that we consider development charges are overrated in high quality worth performs. We state this as a result of so long as Franklin can register sufficient gross sales to provide sustained earnings and money circulation, then this exact same money circulation can be utilized to construct the enterprise by sound acquisitions over time. Free money circulation is a very powerful metric in finance and the motive force of long-term development. Suffice it to say, with a really engaging ahead cash-flow a number of of seven.17, Franklin continues to have the ammunition to stay on the reducing fringe of this ever-evolving trade.

Coated Calls

We then write lined calls on our lengthy inventory place to usher in further earnings alongside the very beneficiant dividend yield. Many see lined name writing as a possibility loss (as a result of potential to overlook on substantial beneficial properties) however in shares comparable to Franklin, we consider it’s the prudent play. Why? Properly, if one research the long-term technical chart above, it’s evident that shares have important overhead resistance in play at current. This implies will probably be very tough to check a breakout occurring right here anytime quickly. Suffice it to say, in buying and selling situations comparable to these, capping one‘s beneficial properties is a prudent transfer. Franklin‘s low valuation, robust profitability, and confirmed dividend all scale back draw back threat in our choice. Quite the opposite, upside potential (given the technicals) seems strained at this level which is ok by us so long as we keep on with the above technique. Suffice it to say, the target is to maintain on promoting bare places or lined calls in BEN to constantly scale back the price of the respective basket of shares. A breakout within the share value or a collapse of Franklin‘s implied volatility would make us rethink our method in due time.

Conclusion

Franklin Sources is a confirmed dividend aristocrat which has been struggling these days as a consequence of excessive inflation, rising rates of interest and the continuing battle in Europe. Though we see the inventory more than likely going sideways over the close to time period, Franklin Sources stays a superb earnings play when one takes under consideration the corporate‘s dividend and elevated implied volatility. We look ahead to continued protection.

[ad_2]

Source link