[ad_1]

What developments ought to we search for it we need to establish shares that may multiply in worth over the long run? In an ideal world, we would wish to see an organization investing extra capital into its enterprise and ideally the returns earned from that capital are additionally rising. Put merely, most of these companies are compounding machines, which means they’re frequently reinvesting their earnings at ever-higher charges of return. Talking of which, we observed some nice modifications in Euromedis Groupe’s (EPA:ALEMG) returns on capital, so let’s take a look.

Return On Capital Employed (ROCE): What’s it?

If you have not labored with ROCE earlier than, it measures the ‘return’ (pre-tax revenue) an organization generates from capital employed in its enterprise. The formulation for this calculation on Euromedis Groupe is:

Return on Capital Employed = Earnings Earlier than Curiosity and Tax (EBIT) ÷ (Whole Property – Present Liabilities)

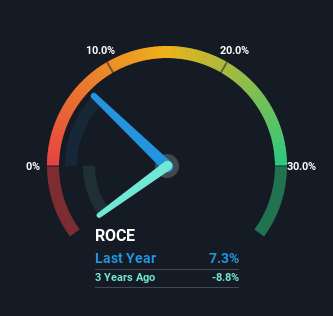

0.073 = €4.3m ÷ (€73m – €13m) (Primarily based on the trailing twelve months to December 2021).

So, Euromedis Groupe has an ROCE of seven.3%. By itself, that is a low determine however it’s across the 6.2% common generated by the Medical Tools trade.

View our latest analysis for Euromedis Groupe

Within the above chart now we have measured Euromedis Groupe’s prior ROCE in opposition to its prior efficiency, however the future is arguably extra essential. In the event you’re , you possibly can view the analysts predictions in our free report on analyst forecasts for the company.

The Pattern Of ROCE

We’re glad to see that ROCE is on track, even whether it is nonetheless low in the meanwhile. Over the past 5 years, returns on capital employed have risen considerably to 7.3%. The corporate is successfully making more cash per greenback of capital used, and it is price noting that the quantity of capital has elevated too, by 72%. This may point out that there is loads of alternatives to speculate capital internally and at ever greater charges, a mixture that is widespread amongst multi-baggers.

Yet another factor to notice, Euromedis Groupe has decreased present liabilities to 18% of complete property over this era, which successfully reduces the quantity of funding from suppliers or short-term collectors. This tells us that Euromedis Groupe has grown its returns with out a reliance on rising their present liabilities, which we’re very proud of.

The Key Takeaway

All in all, it is terrific to see that Euromedis Groupe is reaping the rewards from prior investments and is rising its capital base. Astute traders might have a possibility right here as a result of the inventory has declined 36% within the final 5 years. That being the case, analysis into the corporate’s present valuation metrics and future prospects appears becoming.

Euromedis Groupe does have some dangers although, and we have noticed 4 warning signs for Euromedis Groupe that you just is perhaps concerned with.

Whereas Euromedis Groupe is not incomes the best return, try this free list of companies that are earning high returns on equity with solid balance sheets.

Have suggestions on this text? Involved in regards to the content material? Get in touch with us straight. Alternatively, e mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is common in nature. We offer commentary based mostly on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles are usually not meant to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your targets, or your monetary state of affairs. We goal to carry you long-term targeted evaluation pushed by basic knowledge. Be aware that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link