[ad_1]

Legendary fund supervisor Li Lu (who Charlie Munger backed) as soon as mentioned, ‘The most important funding danger just isn’t the volatility of costs, however whether or not you’ll undergo a everlasting lack of capital.’ After we take into consideration how dangerous an organization is, we all the time like to have a look at its use of debt, since debt overload can result in smash. We be aware that Bhartiya Worldwide Ltd. (NSE:BIL) does have debt on its steadiness sheet. However the true query is whether or not this debt is making the corporate dangerous.

Why Does Debt Convey Danger?

Debt and different liabilities change into dangerous for a enterprise when it can not simply fulfill these obligations, both with free money stream or by elevating capital at a beautiful value. In the end, if the corporate cannot fulfill its authorized obligations to repay debt, shareholders may stroll away with nothing. Nevertheless, a extra widespread (however nonetheless painful) situation is that it has to lift new fairness capital at a low value, thus completely diluting shareholders. Having mentioned that, the commonest scenario is the place an organization manages its debt fairly nicely – and to its personal benefit. The very first thing to do when contemplating how a lot debt a enterprise makes use of is to have a look at its money and debt collectively.

View our latest analysis for Bhartiya International

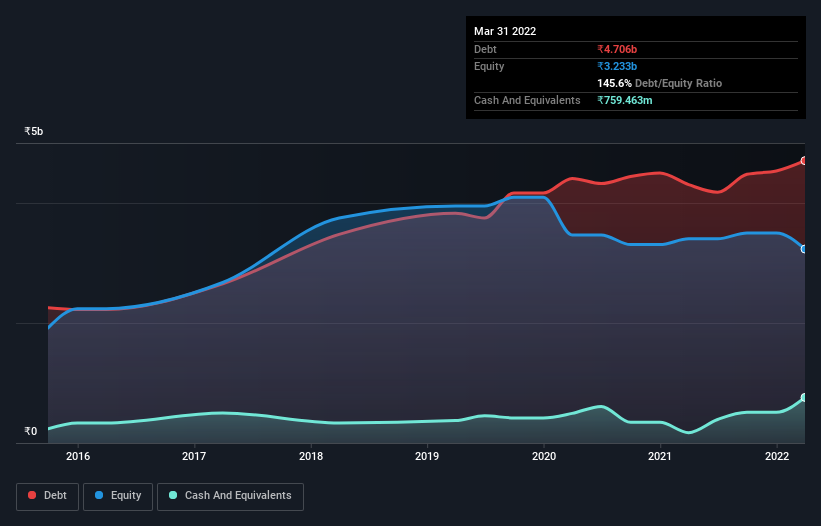

What Is Bhartiya Worldwide’s Debt?

You possibly can click on the graphic under for the historic numbers, nevertheless it exhibits that as of March 2022 Bhartiya Worldwide had ₹4.71b of debt, a rise on ₹4.31b, over one yr. Nevertheless, it additionally had ₹759.5m in money, and so its internet debt is ₹3.95b.

How Robust Is Bhartiya Worldwide’s Steadiness Sheet?

In accordance with the final reported steadiness sheet, Bhartiya Worldwide had liabilities of ₹4.37b due inside 12 months, and liabilities of ₹1.82b due past 12 months. Offsetting this, it had ₹759.5m in money and ₹1.33b in receivables that had been due inside 12 months. So its liabilities whole ₹4.11b greater than the mix of its money and short-term receivables.

This deficit casts a shadow over the ₹2.27b firm, like a colossus towering over mere mortals. So we positively assume shareholders want to look at this one carefully. On the finish of the day, Bhartiya Worldwide would in all probability want a serious re-capitalization if its collectors had been to demand reimbursement.

With a view to dimension up an organization’s debt relative to its earnings, we calculate its internet debt divided by its earnings earlier than curiosity, tax, depreciation, and amortization (EBITDA) and its earnings earlier than curiosity and tax (EBIT) divided by its curiosity expense (its curiosity cowl). Thus we think about debt relative to earnings each with and with out depreciation and amortization bills.

Weak curiosity cowl of 0.50 instances and a disturbingly excessive internet debt to EBITDA ratio of 11.1 hit our confidence in Bhartiya Worldwide like a one-two punch to the intestine. The debt burden right here is substantial. Worse, Bhartiya Worldwide’s EBIT was down 47% over the past yr. If earnings proceed to observe that trajectory, paying off that debt load shall be more durable than convincing us to run a marathon within the rain. There isn’t any doubt that we be taught most about debt from the steadiness sheet. However you’ll be able to’t view debt in whole isolation; since Bhartiya Worldwide will want earnings to service that debt. So if you happen to’re eager to find extra about its earnings, it could be value testing this graph of its long term earnings trend.

Lastly, a enterprise wants free money stream to repay debt; accounting income simply do not minimize it. So we all the time examine how a lot of that EBIT is translated into free money stream. Within the final three years, Bhartiya Worldwide created free money stream amounting to 11% of its EBIT, an uninspiring efficiency. For us, money conversion that low sparks a bit paranoia about is potential to extinguish debt.

Our View

To be frank each Bhartiya Worldwide’s EBIT progress charge and its observe file of staying on prime of its whole liabilities make us quite uncomfortable with its debt ranges. And even its internet debt to EBITDA fails to encourage a lot confidence. It appears to us like Bhartiya Worldwide carries a big steadiness sheet burden. When you play with hearth you danger getting burnt, so we might in all probability give this inventory a large berth. When analysing debt ranges, the steadiness sheet is the plain place to begin. However in the end, each firm can include dangers that exist outdoors of the steadiness sheet. As an illustration, we have recognized 4 warning signs for Bhartiya International (2 are significant) you ought to be conscious of.

When all is claimed and carried out, typically its simpler to concentrate on firms that do not even want debt. Readers can entry a list of growth stocks with zero net debt 100% free, proper now.

Have suggestions on this text? Involved in regards to the content material? Get in touch with us instantly. Alternatively, e-mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is common in nature. We offer commentary primarily based on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles aren’t meant to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary scenario. We purpose to convey you long-term targeted evaluation pushed by basic knowledge. Word that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link