[ad_1]

With its inventory down 15% over the previous three months, it’s straightforward to ignore SoftTech Engineers (NSE:SOFTTECH). We, nevertheless determined to review the corporate’s financials to find out if they have something to do with the value decline. Lengthy-term fundamentals are often what drive market outcomes, so it is value paying shut consideration. Notably, we shall be taking note of SoftTech Engineers’ ROE right now.

ROE or return on fairness is a great tool to evaluate how successfully an organization can generate returns on the funding it obtained from its shareholders. Merely put, it’s used to evaluate the profitability of an organization in relation to its fairness capital.

View our latest analysis for SoftTech Engineers

How To Calculate Return On Fairness?

Return on fairness could be calculated by utilizing the components:

Return on Fairness = Internet Revenue (from persevering with operations) ÷ Shareholders’ Fairness

So, primarily based on the above components, the ROE for SoftTech Engineers is:

5.5% = ₹47m ÷ ₹844m (Based mostly on the trailing twelve months to March 2022).

The ‘return’ refers to an organization’s earnings during the last yr. That signifies that for each ₹1 value of shareholders’ fairness, the corporate generated ₹0.06 in revenue.

Why Is ROE Vital For Earnings Progress?

So far, now we have realized that ROE measures how effectively an organization is producing its earnings. Relying on how a lot of those earnings the corporate reinvests or “retains”, and the way successfully it does so, we’re then in a position to assess an organization’s earnings progress potential. Typically talking, different issues being equal, companies with a excessive return on fairness and revenue retention, have a better progress fee than companies that don’t share these attributes.

SoftTech Engineers’ Earnings Progress And 5.5% ROE

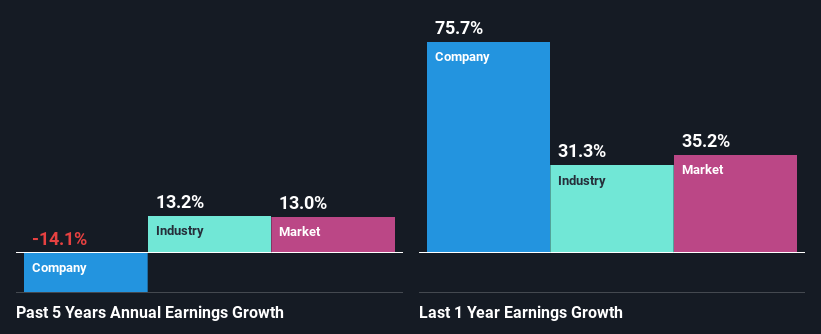

It’s fairly clear that SoftTech Engineers’ ROE is relatively low. Even when in comparison with the business common of 9.9%, the ROE determine is fairly disappointing. Because of this, SoftTech Engineers’ 5 yr internet earnings decline of 14% isn’t a surprise given its decrease ROE. We imagine that there additionally is likely to be different facets which are negatively influencing the corporate’s earnings prospects. For instance, the enterprise has allotted capital poorly, or that the corporate has a really excessive payout ratio.

So, as a subsequent step, we in contrast SoftTech Engineers’ efficiency in opposition to the business and have been disillusioned to find that whereas the corporate has been shrinking its earnings, the business has been rising its earnings at a fee of 13% in the identical interval.

The idea for attaching worth to an organization is, to a terrific extent, tied to its earnings progress. It’s necessary for an investor to know whether or not the market has priced within the firm’s anticipated earnings progress (or decline). By doing so, they may have an thought if the inventory is headed into clear blue waters or if swampy waters await. In case you’re questioning about SoftTech Engineers”s valuation, try this gauge of its price-to-earnings ratio, as in comparison with its business.

Is SoftTech Engineers Effectively Re-investing Its Income?

Whereas the corporate did payout a portion of its dividend previously, it at present would not pay a dividend. This suggests that probably all of its earnings are being reinvested within the enterprise.

Abstract

General, now we have blended emotions about SoftTech Engineers. Whereas the corporate does have a excessive fee of revenue retention, its low fee of return might be hampering its earnings progress. Wrapping up, we might proceed with warning with this firm and a method of doing that may be to take a look at the danger profile of the enterprise. You possibly can see the 4 dangers now we have recognized for SoftTech Engineers by visiting our dangers dashboard totally free on our platform here.

Have suggestions on this text? Involved concerning the content material? Get in touch with us instantly. Alternatively, e mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is basic in nature. We offer commentary primarily based on historic information and analyst forecasts solely utilizing an unbiased methodology and our articles should not supposed to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your aims, or your monetary scenario. We intention to deliver you long-term targeted evaluation pushed by basic information. Notice that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link