[ad_1]

CHUNYIP WONG/E+ by way of Getty Photos

Allegheny got here on the high amongst industrial shares — which additionally included aero-defense firms — in H1 whereas navigating an setting suffering from warfare, rising inflation and fears of recession. In the meantime, Vertiv lead the decliners, which included constructing merchandise makers, as these worst 5 performers noticed greater than 50% erosion of their inventory worth.

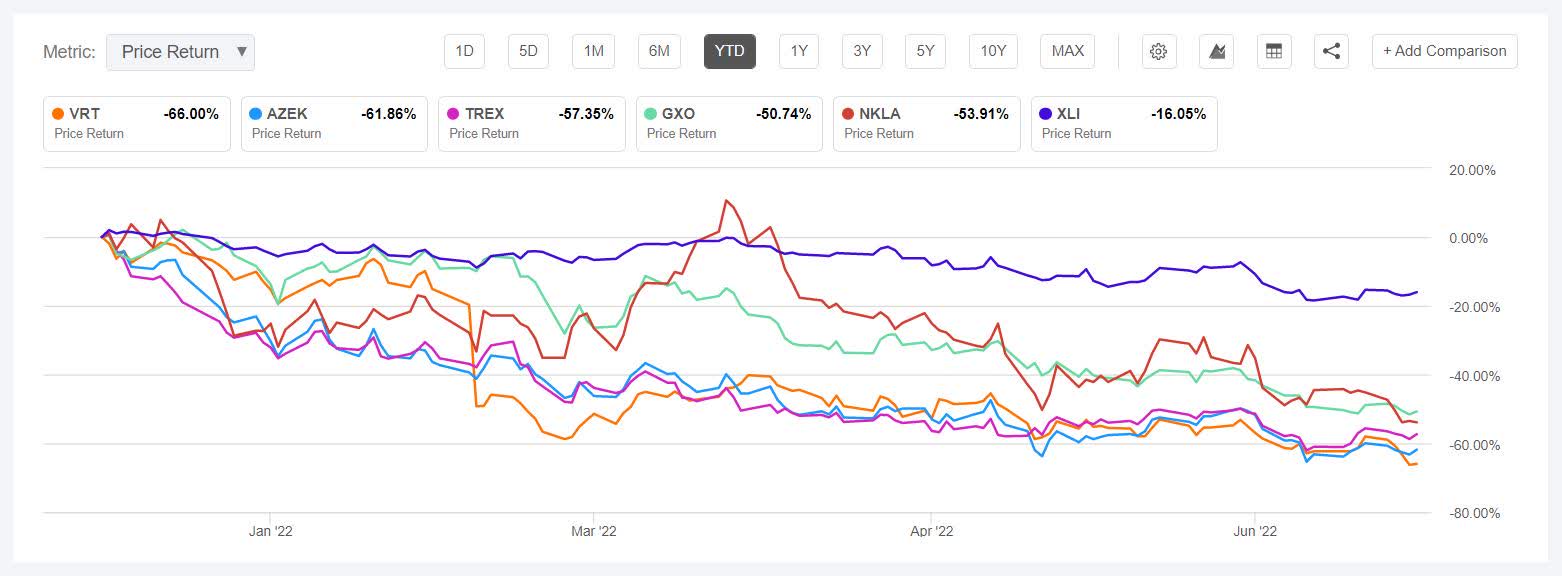

For the primary half of the yr, the SPDR S&P 500 Belief ETF (SPY) finished -19.9%, being within the purple for 4 out of the primary six months of 2022. The Industrial Choose Sector SPDR (XLI) additionally misplaced -16.38%.

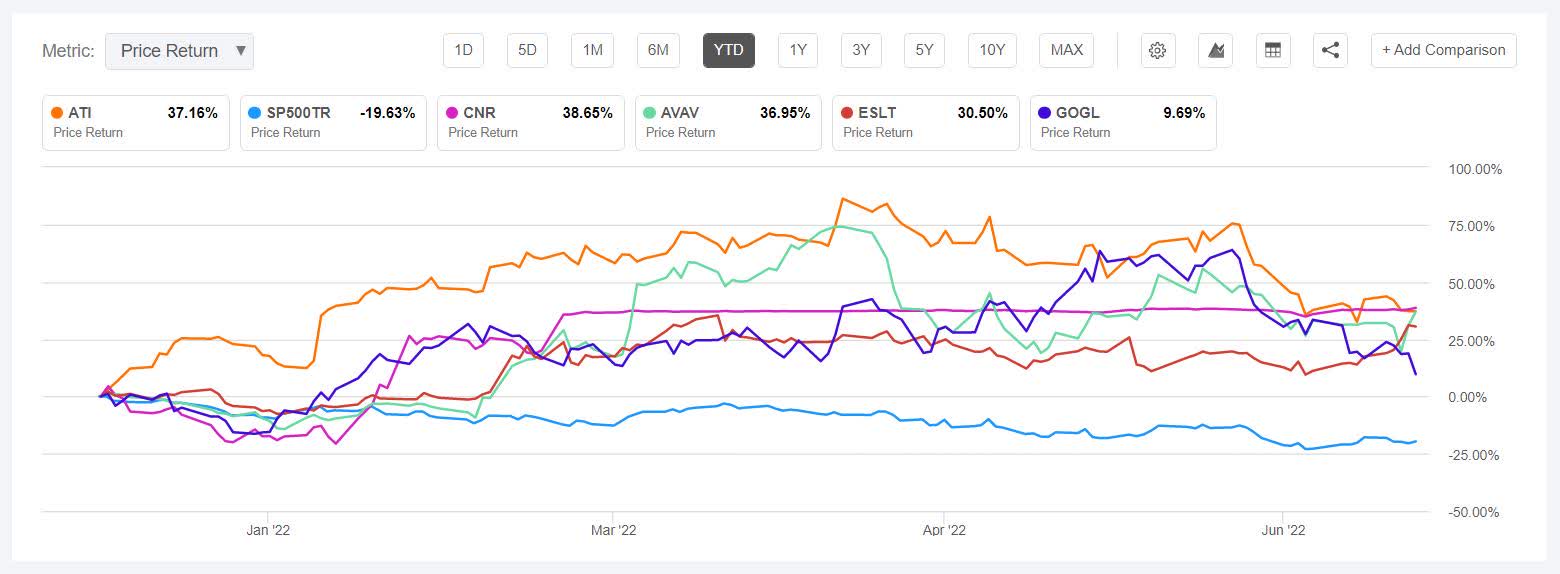

The highest 5 gainers within the industrial sector (shares with a market cap of over $2B) all gained greater than +29% every in H1.

Allegheny Applied sciences (NYSE:ATI) +42.92%. The Pittsburgh, Pa.-based specialty supplies maker’s inventory gained nicely at the beginning of the yr. The inventory was the highest industrial gainer (on this section) in a single week in January and in one other week landed among the many greatest 5. The corporate additionally gained in February, after its This fall results beat analysts’ estimates. The inventory additionally surged on Could 4, after after the corporate reported a +20.4% Y/Y rise in Q1 revenue.

The SA Quant Score on Allegheny is Strong Buy, which which takes into consideration elements corresponding to development and profitability, amongst others issues. The common Wall Road Analysts’ Score can be Strong Buy, whereby 5 out of 8 analysts give it a Sturdy Purchase ranking. SA contributor, Fade The Market wrote in June: Allegheny Applied sciences: Driving The Development.

Cornerstone Constructing Manufacturers (CNR) +40.34%. The Cary, N.C.-based firm’s inventory was the top industrial gainer for 2 weeks in a row in February after experiences surfaced that Clayton, Dubilier & Rice was mulling a proposal to purchase the rest of the corporate it would not already personal. In March CNR agreed to be acquired and brought non-public by the agency in a cope with an enterprise worth of $5.8B.

Wanting forward on the Building sector: Baird up to date its 2022/2023 U.S. Building forecast, with a complete have a look at numerous verticals (Non-public non-residential, Public non-residential, and Residential). Relative to the agency’s December 2021 estimate, it was elevating its 2022 spending development estimate by 100 foundation factors to 7%, whereas decreasing its 2023 estimate because it now forecast a 3% decline (an 11% contraction in Residential, is anticipated to offset ~7% Non-residential development).

The chart under reveals YTD price-return efficiency of the highest 5 gainers and SP500TR:

Aero-defense shares AeroVironment (AVAV) +32.90% and Elbit Methods (ESLT) +31.16%, took the third and fourth spot, respectively, in H1 gainers buoyed amid the Russia-Ukraine warfare.

Drone maker AeroVironment (AVAV) was among the many aero-defense shares being initiated at Berenberg in January. AVAV acquired a Maintain ranking then with a value goal of $66, after greater than 5 months now the inventory has breached the $85 mark. Nonetheless, in April, Baird downgraded inventory to Impartial with a $95 value goal, saying the inventory was “forward of itself” and famous that future Switchblade orders would take time to materialize. However in Could, RBC Capital upgraded AVAV to Outperform noting that the Switchblade drone had considerably reset the corporate’s funding alternative at a better degree. Prior to now six months, AeroVironment has bagged a number of contracts for its Puma line of unmanned aircraft programs. Nonetheless, the corporate’s FQ4 revenue noticed a -2.5% Y/Y decline and it has issued a below-consensus guidance for FY 2023 earnings.

The common Wall Road Analysts’ Score for AVAV is Buy, with an Common Value Goal of $92.5. The ranking is in distinction to the SA Quant Score of Hold, with Valuation and Development each having an element grade of F.

In the meantime, Elbit Methods (ESLT) completed the week ending July 1 on a excessive, because the inventory was the top industrial gainer (on this section). ESLT was additionally among the many high 5 gainers in June. In H1 2022, the corporate secured round 10 contracts that we all know of, notables being: a $548M contract with a rustic within the Asia-Pacific area; a ~$130M deal to ship an artillery munitions manufacturing line; a $220M contract to produce precision steering kits for airborne munitions. The SA Quant Rating and the typical Wall Road Analysts’ Rating, on ESLT is Maintain.

Golden Ocean Group (GOGL) +29.48%. The Bermuda-based delivery firm noticed first rate positive aspects from February until the beginning of June (see chart here). The corporate was the highest industrial gainer for per week in April. GOGL additionally rose in Could following its Q1 earnings beat, and a robust forecast for the quarters forward. The inventory nonetheless has hit tough waters for the reason that second week of June, amid a world worry of recession and impact on container demand. The SA Quant Score on GOGL is a Strong Buy, whereas the typical Wall Road Analysts’ Score is Buy.

H1 high 5 decliners amongst industrial shares (market cap of over $2B) all misplaced greater than -51% every.

Vertiv (NYSE:VRT) -67.12%. The final week of June summed up the the inventory’s misfortune, as for the week ending July 1, VRT was the worst performer (on this section). The inventory crashed 40% following its This fall results in February, whereby income missed Road estimates. The Ohio-based firm, which gives tools and providers to knowledge facilities, had additionally famous that offer chain headwinds would persist by 2022. (See chart here). The SA Quant Score on the inventory is Hold, which in distinction to the typical Wall Road Analysts’ Score of Buy.

Constructing merchandise makers Azek (AZEK) -63.27% and Trex (TREX) -59.50%, got here within the second and third spot for H1 worst decliners.

Each Azek and Trex noticed a downgrade in April at Loop Capital to Maintain from Purchase on the idea of a muted mid-term outlook. Nonetheless, in June BofA Securities upgraded Azek to Purchase noting that the inventory’s valuation has de-rated versus constructing merchandise group and development potential was compelling.

The SA Quant Score on AZEK is Sell, with Profitability having an element grade of C- and Momentum having a D- issue grade. The ranking is in distinction to the typical Wall Road Analysts’ Score of Strong Buy, whereby 12 out of 19 analysts give the inventory a Sturdy Purchase ranking.

In the meantime, the typical Wall Road Analysts’ Score for TREX is Buy, with an Common Value Goal of $75.82. The ranking is in distinction to the SA Quant Score of Hold, with Development having a C+ issue grade and Momentum with an element grade of D.

The chart under reveals YTD price-return efficiency of the worst 5 decliners and XLI:

Greenwich, Conn.-based GXO Logistics (GXO) declined -52.21% in H1. However the common Wall Road Analysts’ Score is Buy, with an Common Value Goal of $82.93. 9 out of 15 analysts give it a Sturdy Purchase ranking. In Could CNBC commentator Stephen Weiss was bullish on GXO. The inventory, nonetheless, has continued to say no (see chart here). In February, GXO stated it was acquiring Clipper Logistics in a deal price ~$1.26B.

Nikola (NKLA) -51.82%. The electrical car maker was the worst performing industrial inventory in June and Q2 (on this section), declining -33% and -57%, respectively. Nikola’s inventory began trending downwards after mid-January, earlier than attempting to choose up at March finish (see chart here) however then once more declining from April. March started with Auto shares falling on anxiousness over the impact of Russia’s assault on Ukraine. The common Wall Road Analysts’ Score is Hold, which is in distinction to the SA Quant Score of Sell.

Wanting forward on the Auto sector: Baird now modelled international auto manufacturing +3% in 2022, versus its earlier estimate of +5%. Main elements thought of by the agency included outsized chip affect on Japanese and Korean auto manufacturing, whereas it additionally fine-tuned North America (conservatism), Europe (attributable to Russia/Ukraine warfare) and China (attributable to lockdowns).

Wanting forward on the Rental sector: Baird notes that FY23 U.S. rental income steering development appear to be completely pushed by fleet growth. The agency famous that H1 2022 could be remembered as among the best durations for tools rental fundamentals. Baird added that it remained agency in its view that business tools provide/demand dynamics are ready to shift in H2 2022 and into 2023 which may average rental charges and income development/margins.

[ad_2]

Source link